When applying for a home loan, one of the most important financial components to understand is the loan to value ratio (LVR). Why, you may ask. It’s because LVR plays a major role in determining how much you can borrow, and the interest rate you may receive, and whether you will need to pay Lenders Mortgage Insurance (LMI).

Loan to value ratio measures the relationship between the amount you want to borrow from a lender and the value of the property you intend to purchase. Lenders commonly use this ratio to assess the level of risk involved in approving your loan. The higher the LVR, the greater the perceived risk to the lender.

Save interest by paying off your mortgage faster!

For instance, if a borrower has a small deposit and needs to borrow most of the property’s value, the lender faces a higher risk of the borrower not being able to repay the loan, considering that they already have limited funds. As a result, lenders closely monitor LVR when evaluating mortgage applications. In several cases, an LVR above 80% is considered a higher risk.

The size of your deposit plays a massive role in determining your loan to value ratio. A larger deposit automatically reduces the amount you need to borrow, which reduces your LVR and also the lender’s risk. Because of this, borrowers with lower LVRs, which typically means LVRs lower than 80, often have access to better and more favourable loan terms.

However, several borrowers, especially first home buyers looking to fund their first home, may not have large deposits saved. For them, securing an LVR under 80 might be difficult. This is where Lenders Mortgage Insurance comes to play. To every LVR of more than 80, LMI is added to the loan.

With owner-builder construction loans, help fund your self-managed build in stages!

Overall, understanding loan to value ratio is essential whether you are buying your first home, investing in property, upgrading to a larger house or refinancing an existing mortgage. Not only does it help you make better financial decisions, but it also creates an outline for a suitable deposit preparation and improves your chances of home loan approval.

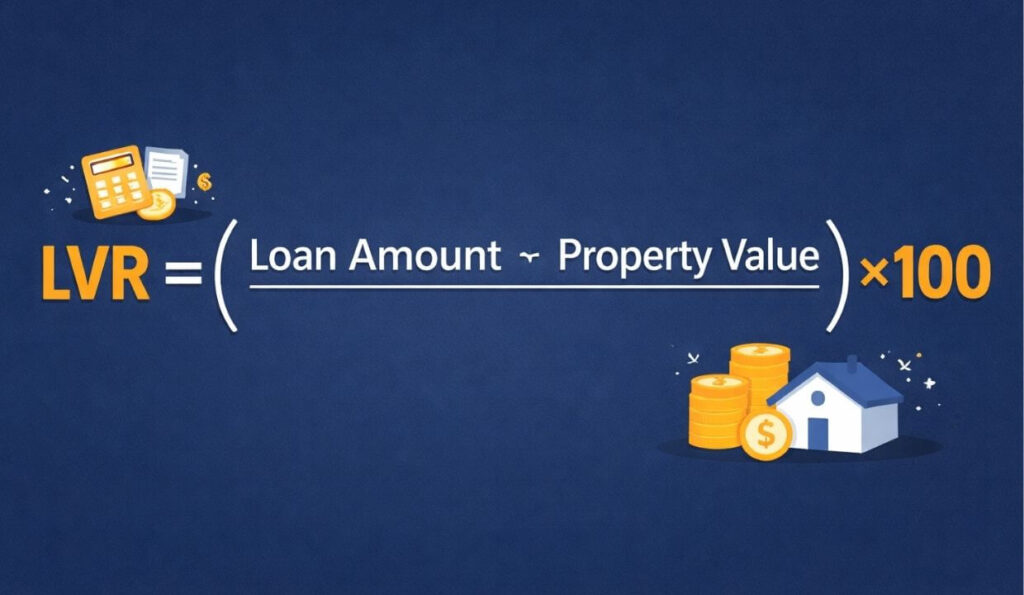

Loan to Value Ratio Formula

Loan to value ratio (LVR) is calculated by comparing the amount you intend to borrow with the lender-assessed property valuation, and the result is then expressed as a percentage.

Please note that the lender’s valuation of a property may differ from the purchase price or market value. Banks usually rely on their own independent valuation when calculating LVR.

Did you know you could use super to buy your first home?

LVR Formula:

LVR = (Loan Amount ÷ Property Value) x 100

Here, the formula shows the proportion of the property’s value that is being financed through a loan. The remaining percentage after calculation represents the deposit or equity contributed by the borrower.

Try debt recycling to turn home loan debt into tax-deductible debt!

Loan to Value Ratio Example

Consider a couple, Ash and Eiji, who are planning to purchase a property. Perhaps a first home.

The bank’s valuation of their home is $1,000,000, and they intend to borrow $800,000. This means they would contribute a $200,000 as part of their deposit.

To calculate loan to value ratio, you need to:

- Divide the loan amount by the property value

- Convert the result into a percentage

So, $800,000 ÷ $1,000,000 = 0.8 and 0.8 x 100 = 80%. Therefore, Ash and Eiji have an LVR of 80%, indicating that their loan covers 80% of the property’s value while their deposit accounts for the remaining 20%.

Buy a new home before selling your current one with Bridge loans!

But what if they aren’t able to accumulate enough for their property purchase and need to borrow more? If they decide to borrow $900,000 instead of $800,000, their LVR would increase.

So, $900,000 ÷ $1,000,000 x 100 = 90%

Because the ratio exceeds the needed 80% threshold to avoid lender’s mortgage insurance, they may need to pay the required LMI as part of their home loan.

Rent wherever you want while investing where you can afford by rentvesting!

The larger your deposit, the lower your LVR will be. A low loan to value ratio is considered less risky for lenders because the borrower has invested more of their own funds into the property. This reduces the likelihood of financial loss for the lender in case the borrower is unable to meet their loan repayments.

Ultimately, understanding LVR can help borrowers plan their deposits more effectively and anticipate potential costs associated with higher LVR loans.

Calculate rental yield to find your real profit after expenses on your property investment!

Why is LVR Important in a Home Loan Application?

- Risk Assessment for Lenders: Banks and lenders typically use LVR to measure the risk on a loan. A higher LVR indicates that you are borrowing a larger portion of the property’s value, which increases the lender’s risk. Whereas a lower LVR indicates lower risk, due to the borrower’s own contribution to the property budget.

- Impact on Interest Rates and Loan Terms: Several lenders are known to implement tiered pricing based on the loan to value ratio percentages. For example, for an LVR ratio below 60%, you qualify for the lowest interest rates due to lower risk. For LVR between 60 and 80%, borrowers may attract slightly higher interest rates, but they’re still considered relatively low risk. However, an LVR above 80% is generally considered high risk, which can result in higher interest rates or additional costs.

- Lenders’ Mortgage Insurance: If your LVR exceeds 80%, lenders may require lenders mortgage insurance to protect themselves in case of a default. LMI is a one-time premium that can be added to the loan or paid up front. This is one way for lenders to save themselves when increased risk is posed by high LVR loans. Try using our LMI calculator for accurate LMI payment estimates!

- Guarantors as an Option: For borrowers with high LVRs, a family member can act as a guarantor, offering the required security for part of the loan. This can reduce the LVR from the lender’s perspective, potentially avoiding LMI while securing better interest rates.

- Influence Borrowing Capacity: When your LVR is low, you have a chance of increasing your borrowing capacity. Lenders are more willing to lend higher amounts at favourable rates when you have a substantial deposit or equity, reducing the overall cost of borrowing.

If you are self-employed and looking for a non-traditional home loan option, low-doc home loans might be just the choice for you!

Maintaining a low LVR is advantageous because it reduces your loan risk and can land you lower interest rates while helping you avoid additional insurance costs. Understanding loan to value ratio and how it impacts loan terms is key to successfully securing a home loan.

Find out how to secure a property without an upfront deposit with Deposit Bonds!

The Cons of High LVR Loans

Along with paying the LMI, there are several other reasons why higher interest rates are disadvantageous and prove to be a high risk for lending.

- Increased Financial Risk: A high LVR means less deposit, and with your personal contribution limited in your property, you naturally have less equity. In this circumstance, if you’re unable to meet your repayments, the lender may need to sell the property to recover the loss. Toward the end, you, as a borrower, will have nothing to your name.

- Higher Interest Rates: Lenders generally charge higher interest rates on high loan-to-value ratio loans. This is to offset the risk of lending and position the transaction at a balance. While interest rates can change over time, a higher LVR typically means you’ll pay more in interest over the life of the loan. Try using our home loan repayment calculator to understand how different interest rates affect your monthly payments.

- Hefty Repayments: When interest rates are high, larger monthly repayments are to be expected. If LMI is added to the loan amount, your repayments will increase even more.

- Strict Application Criteria: Applications with high LVRs are often examined more carefully by lenders. They want to ensure that borrowers can meet regular repayments even under financial stress, making the home loan approval process slightly more rigorous.

Benefits of a Lower LVR

There are several advantages to maintaining a low LVR, which is usually 80% or below. Some include:

- Low interest rates: The reduced risk allows lenders to offer better interest rates.

- Lower Repayments: Less interest and no LMI means your monthly repayments are substantially lower.

- Better Borrowing Capacity: A larger deposit improves your borrowing power. Use our borrowing power calculator for easy home loan budgeting!

- Easier Approval Process: Since low LVR loans are less risky, lenders view such applications with much less scrutiny.

Are you a single parent looking to buy a home? The Family Home Guarantee Scheme is specifically made for eligible single guardians!

How to Reduce Your Loan to Value Ratio?

You should already know how reducing your loan-to-value ratio (LVR) can help you secure a home loan with low interest rates. Along with that, not only can you avoid the lender’s mortgage insurance (LMI) but also improve your overall financial position. Here are some practical ways to lower your LVR:

- Build a Larger Deposit: The most straightforward way to reduce your loan to value ratio is to save a large deposit. The more you can contribute upfront, the smaller your loan relative to the property value. Aiming for a deposit that brings your LVR below 80% can make you eligible for lower interest rates and help avoid LMI premiums.

- Choose a Cheaper Property: Buying a property with a lower purchase price allows you to achieve a lower LVR without increasing your deposit. This approach can help you enter the property market sooner, giving you a foothold while maintaining manageable debt levels.

- Get a Guarantor for Your Home Loan: In this case, getting help from a family member can also be a good way out. When a family member acts as a guarantor for your home loan, they use the equity in their home to support your loan. This can reduce your LVR from the lender’s perspective and could also help you avoid LMI.

- Negotiate Property Valuation: Sometimes, lenders may reassess the property valuation if market conditions have improved. In the meantime, if your property valuation has gone higher compared to your loan amount, your LVR can be reduced.

What Costs are Not Included in the Loan Amount When Calculating LVR?

When your LVR is calculated, the loan amount and the property value are considered. However, there are numerous other upfront costs involved in buying a home that are not included in the loan amount. These costs are expected to be paid out of your own savings and should be budgeted in when planning for your deposit.

Find out what happens on settlement day to avoid mishaps and stress!

Some upfront costs not included in the loan amount are:

- Stamp Duty

- Legal and Conveyancing Fees

- Building Valuations and Inspection

- Loan Application Fees and Charges

Since these expenses are paid separately, there’s a high chance that they can reduce the amount available for your deposit. If you don’t plan for them properly, your deposit can wind up being smaller than expected, which means a high LVR. Therefore, you should carefully account for these additional costs when saving for a home.

Rent now with the option to buy later with Australian Rent to Buy Schemes!

What’s the Maximum Loan to Value Ratio I Can Have?

The maximum LVR you can have to be approved for a home loan depends mostly on the lender’s policies and your individual circumstances. There are also factors such as your income, credit history, employment stability and the purpose of purchase that determine how much you can borrow. However, typical standards reveal that up to 90% LVR is still acceptable. Many lenders cap borrowing at this level, which means that you will need at least a 10% deposit.

It is extremely rare for lenders to allow loan-to-value ratios over 90, but some lenders allow higher LVRs, enabling you to purchase your property with as little as a 5% deposit, but this benefit comes with higher repayments and costs, including lender’s mortgage insurance.

Ultimately, it is possible to borrow with a high LVR, but most borrowers aim for 80% or lower to avoid LMI and access better loan terms.

Find out how mortgage works after your divorce!

How is the Property Value Assessed When Calculating the LVR?

As you’re already aware, when calculating your loan-to-value ratio (LVR), lenders rely on property valuations to determine how much your property is worth. There are two main types of valuations used in the process:

- Market Valuation: A market valuation is an estimate of the price your property would likely sell for in the current market. This value is typically provided by real estate agents, based on recent sales of similar properties.

- Bank Valuation: A bank valuation is typically conducted by a qualified, independent valuer who is appointed by the lender. This valuation is more conservative compared to a market valuation and takes into account factors including location, condition, property features and market risks.

Please note that if there happens to be a difference between the market valuation and bank valuation, the lender is likely to use the lower of the two values to calculate your loan to value ratio.

Wondering whether getting a mortgage broker might be right for you? Read our piece on the pros and cons of using a mortgage broker to weigh your options and opinions!

What is a Good Loan to Value Ratio?

A good loan-to-value ratio in Australian standards, much like elsewhere, is typically considered to be 80% or lower. This indicates that you have atleast 20% deposit or equity in the property, which means a lesser chance of you defaulting on loan repayments.

Not only does the LVR of 80 per cent protect the lenders, but it’s also extremely advantageous for borrowers. You can achieve competitive rates with low LVRs and also avoid the lender’s mortgage insurance. The home loan approval process is more manageable, and you start with a larger ownership stake in your property, which would have been impossible with a high loan-to-value ratio.

Refinancing and LVR

If you choose to refinance your home loan, your lender will typically arrange a new valuation of your property. The value of your home may have either increased or decreased since you originally purchased it, so this step is irreplaceable. In the end, your loan-to-value ratio will be recalculated based on the lender’s current assessed value, not the original purchase price.

Similar: Refinancing a Home Loan with Bad Credit.

Loan to value ratio not only determines your eligibility for refinancing but also impacts the process of home equity access in case you’re looking to access your home equity through a cash-out refinance. The more equity you have, the more flexibility you may have to borrow additional funds. Therefore, understanding loan to value ratio is absolutely essential even when refinancing.

For personalised guidance on managing or landing the perfect home loan, feel free to reach out to Nice Loans, your trusted mortgage broker in Brisbane! Our team can provide tailored advice to help you make informed decisions and potentially save thousands on your loan!