Home loan portability, also known as substitution of security, is a home loan feature that allows you to keep the same mortgage loan product while simply changing the supporting security. In simpler terms, portability here refers to the transfer of your existing mortgage from one property to another without needing to refinance your home loan.

The process aims to save not only your time and effort but also the costs associated with applying for a new loan. While the expenses associated are generally lower than full refinancing costs, it’s important to understand that there still are miscellaneous fees and charges involved when going through with a loan portability application.

Read: How to Get a Home Loan If You’re Self Employed?

Moving homes is not an uncommon occurrence. Within a typical 30-year mortgage term, you can see people looking to move once or sometimes even twice. Without loan portability, this would often mean refinancing every time you move, which can be both costly and time-consuming.

Using a portability loan, you can take your existing mortgage with you when you move, keeping your current interest rate. It is a hassle-free solution for homeowners looking to upgrade, downsize or relocate without disrupting their financial set-up.

Try property investment to boost heavy returns!

How Does a Loan Portability Application Work?

As mentioned, loan probability allows you to transfer your existing mortgage from one property to another without changing the loan product itself. While it originally existed to help borrowers avoid exit fees, previously charged when refinancing or switching loans, it has remained a standard and valuable feature even after the fees were removed.

The functional aspect of loan portability applications is as simple as the very definition, it enables one to move their current loan, along with its balance, interest rate and features such as an offset account or redraw facility to a new property. This means you don’t need to start from scratch with a new home loan application, making the process faster and often more cost-effective.

There are two main ways to use home loan portability, depending on whether you’re buying and selling at the same time or transitioning between properties.

Get a home loan pre-approval and find out exactly how much you can borrow for your home loan!

Same-day Settlement or Simultaneous Settlement

This option is ideal when you are buying a new property while selling your current one at the same time. It allows for a smooth and immediate transfer of your loan security.

Rent wherever you want while investing where you can afford by rentvesting to boost your overall capital growth!

In this scenario, your existing property is currently held as security against your loan, the settlement dates for both the sale and purchase of your properties are aligned, and the loan security is transferred directly from your old property to the new one.

To proceed, you’ll need to submit a portability application before finalising the sale or purchase. Your lender will typically require the sales contract for the new property. Throughout the process, you should continue making your regular home loan repayments as usual.

Fund your self-managed build in stages with owner builder home loans!

Deferred Settlement

Deferred settlement applies only when you’ve sold your property but haven’t purchased or settled on a new one. In this case, the proceeds from the sale of your property are placed into a term deposit. The said home loan deposit temporarily acts as security for your loan, and the whole arrangement usually lasts up to 6 months, or up to 3 months in case Lenders Mortgage Insurance applies.

Once you’ve secured and are ready to settle on a new property, the term deposit is closed, and the new property becomes the security for your loan.

It’s important to note that to use this option, you must apply for loan portability before selling your current property. Once you find a new property, you’ll need to provide your lender with the purchase contract to complete the process. As with all home loan probability arrangements, you must continue making your regular loan repayments during this period.

Did you know that you can buy your dream home with zero deposit?

How Do You Qualify?

Qualifying for home loan portability mostly depends on your lender’s specific criteria, but several common requirements and restrictions apply to most loan portability applications. Understanding these conditions can help determine whether a portability loan is the right home loan for your situation.

For borrowers opting for simultaneous settlement, some lenders require that the exchange and settlement of both properties occur on the same day. This ensures a seamless transfer of security under your loan portability arrangement.

However, not all lenders enforce this rule, so flexibility may vary depending on your provider.

You need to make sure that the property you intend to purchase meets your lender’s standards. This means it must be considered suitable for security in terms of location, property type and market performance. If the property does not meet the provided criteria, your portability application may be declined.

Figure out whether to negatively or positively gear your investment property for maximum profit!

Apart from the property type, what also matters is property valuation. Valuation plays a key role in home loan portability. Lenders typically require your new property to be of equal or greater value than your existing one, or that the loan remains within acceptable risk limits. If the valuations don’t meet expectations, you may need to adjust your loan or contribute additional funds.

In several cases, it is advised that the loan amount remain the same when using a portability loan. However, some lenders may allow you to increase or add to your loan if you need additional funds to complete your property purchase. If you happen to increase, you need to go through a separate approval process before your loan portability application is finalised.

Lastly, a critical factor in determining your eligibility is your loan-to-value ratio (LVR). If your LVR exceeds 80% of the new property’s value, you may be required to pay Lenders Mortgage Insurance (LMI). A lower LVR signifies financial strength and stability, thus improving your chances of home loan approval and reducing additional costs.

Overall, meeting all the provided criteria strengthens your chances of a successful portability application. Since lender policies can vary, it’s always a good idea to review your options carefully or seek professional advice before proceeding with loan portability.

Pros and Cons of Home Loan Portability

Home loan portability is a feature that allows you to keep your current home loan while buying and selling property by substituting the security attached to your loan. A portability loan can offer significant time and cost savings, but like any financial decision, it comes with both advantages and potential drawbacks.

Understanding the pros and cons of loan probability will help you make a more informed decision before submitting a portability application.

Use a guarantor on your home loan to boost your home loan approval with a little deposit!

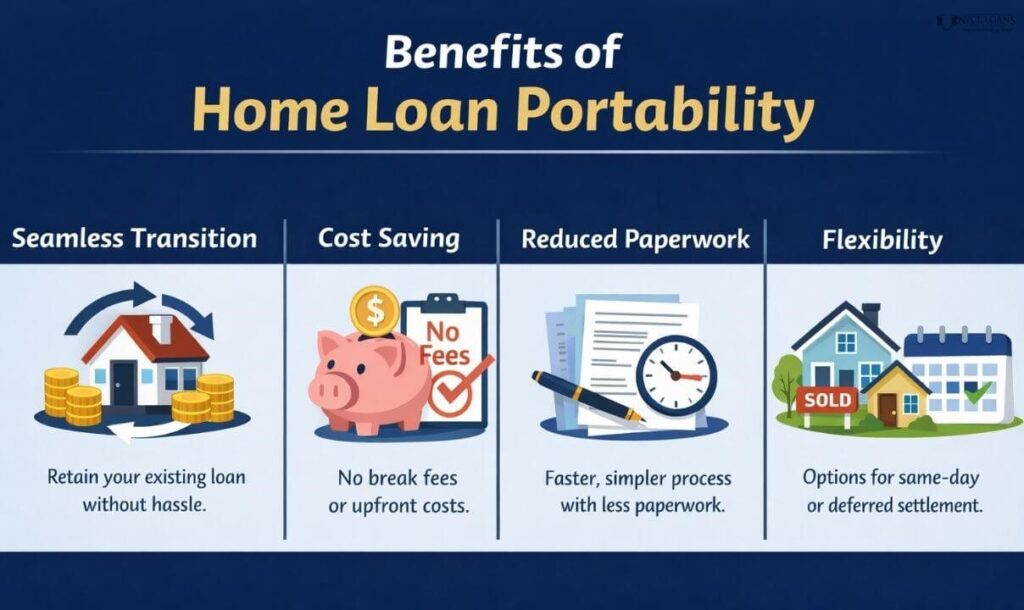

Pros

- Seamless Transition: One of the primary advantages of home loan probability is how it allows seamless continuity. You can retain your existing loan without needing to start over. Not only does your current setup remain unchanged, but the transition is also equally hassle-free. This becomes especially beneficial if you’re on a competitive or fixed rate home loan. You can have access to all the same features, including offset accounts, redraw facilities and direct debit arrangements and won’t lose all the progress you’ve made on repayments either.

- Cost Saving: Since you’re only changing the security (property), not the loan itself, break fees don’t apply. Which means you can avoid application fees, exit fees and other upfront costs associated with a new loan.

- Reduced Paperwork: Unlike with refinancing, where there is one process after another, a loan probability application is usually quicker and simpler. Not only is the processing time low, but paperwork is also reduced.

- Flexibility: Flexibility is also a key benefit. Even if you haven’t found your new property or home, you can still use loan portability. There are several settlement options available, including same-day settlement or deferred settlement.

Find out your rental income after expenses by calculating your rental yield!

Cons

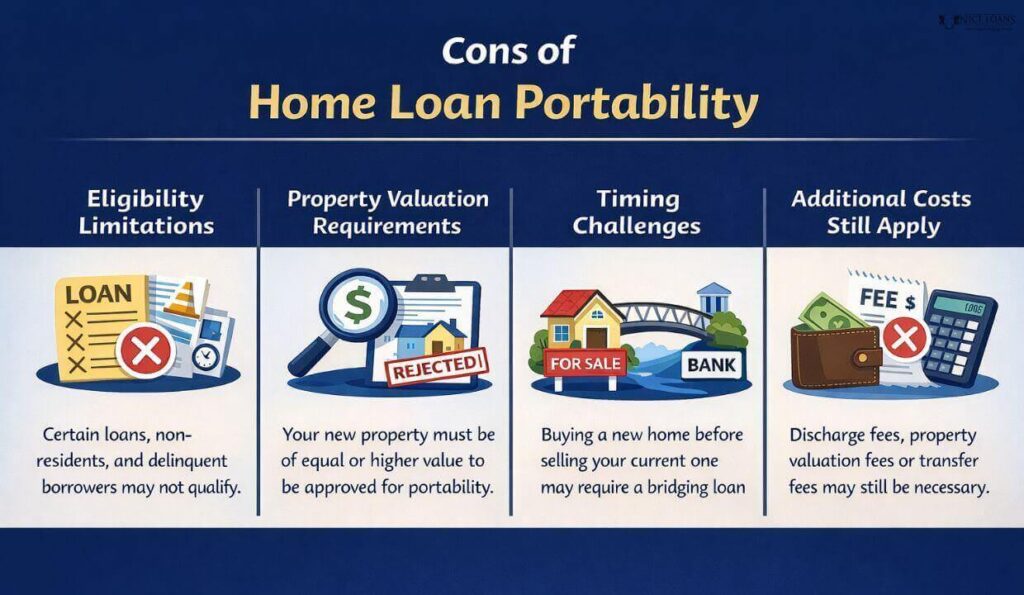

Despite the advantages, loan portability is definitely not for everyone.

- Eligibility Limitations: Not all loans qualify for home loan portability. Common exclusions include construction loans, loans held by non-residents, loans with repayment issues or delinquency history, existing bridging or relocation loans, loans with pending increases that haven’t yet been approved and more.

- Property Valuation Requirements: In case your new property is not of equal or higher value, your portability application may not be approved unless you contribute additional funds or apply for an increase.

- Timing Challenges: If you want to buy a new property before selling your current one, you may need a bridging loan. Once your existing property is sold, you can then proceed with loan portability. Another way to face the inevitable gap is to use deposit bonds, which allow you to purchase a home without a cash deposit!

- Additional Costs Still Apply: Even though a portability loan avoids many refinancing costs, you may still need to pay discharge fees, property valuation fees or transfer fees. However, it is worth noting that although these costs exist, they are generally lower than the expenses involved in refinancing a completely new loan.

Are you self-employed, looking for a flexible home loan? Low doc home loans could be an option for you!

What is the Cost of a Loan Portability Application?

The cost of a loan portability application is generally lower than refinancing, which is one of the key reasons many borrowers consider home loan portability when moving properties. However, there are still some expenses one has to keep in mind.

As a mortgage broker myself, I have long been advising clients. Preparation is key, I tell them, not just in terms of the home loan applications as a whole, which is essential, of course, but also when it comes to the costs that might cause stress in the near future.

Most lenders charge a portability fee of around $200 to transfer your mortgage from one property to another. The good news is that this fee is typically fixed and does not vary, regardless of how much your loan amount might be.

Also Read: Benefits and Risks of Debt Recycling Explained!

What several borrowers overlook is that, apart from the portability fee, you’ll still need to budget for the standard costs associated with buying a new property. This is the preparation I was speaking of. Costs, including those of stamp duty, other legal and administrative costs, are still pending and need to be taken care of.

Another cost to consider is the property valuation fee, which usually ranges from $300 and $600. This is essential for lenders to ensure that the new property meets their security requirements for loan portability.

Speak with your mortgage broker and get help determining the proceeds from the sale of your current property, and if it will be enough to cover these costs, or if you’ll need to pay some expenses out of pocket.

Alternatives to Using the Loan Portability Feature

As convenient and cost-effective as home loan portability is, it can’t be for every borrower. Depending on your needs, there may be better alternatives to consider instead of submitting a portability application.

For instance, you could refinance. In many cases, this approach can be more beneficial than sticking with your current portability loan, especially if market conditions have improved since you first took out your mortgage. You can access better interest rates or updated loan features through refinances. Simply make sure that you’re financially fit, with a good credit score and report, since refinancing with bad credit can be quite difficult.

Another option is simultaneous settlement without portability, where you sell your current property, use the proceeds to pay off your existing loan and take out a new loan for your new property. While this does involve more paperwork than home loan portability, it can give you greater flexibility in restructuring your finances.

If you sell your home before buying a new one, you may be able to use the sale proceeds as temporary security for your loan. This approach can work as an alternative to a deferred loan portability arrangement, depending on your lender’s policies. Remember to carefully compare all available options and decide accordingly.

Rent now with the option to buy later with the Australian rent-to-buy schemes!

Get Expert Advice

Overall, loan portability offers a strong balance of convenience and cost savings, making it a worthwhile option to consider when moving homes. By allowing you to keep your existing loan structure, interest rate, and features, home loan portability simplifies the transition and reduces the financial and administrative burden that might come with refinancing.

Find out how salary sacrifice affects your home loan application!

However, it is also essential to assess whether it is right for you. The benefits being abundant doesn’t mean it isn’t full of drawbacks. Taking the time to evaluate your options will ensure you make the right financial decision.

Get in touch with Nice Loans, the best mortgage broker in Brisbane, to explore all your available options and find the best path forward for your home ownership and financing journey. Whether you’re considering home loan portability or simply looking for the best home loan for your first home, expert guidance can help you make a confident and informed decision.

FAQs

Who is a portability loan fit for?

A portability loan is fit for borrowers who are selling and buying property at the same time, and are happy with their current home loan’s interest rate and features. A portability loan is best for those avoiding the costs and hassle of refinancing.

What type of property can be used for Home Loan Portability?

You need to make sure that the new property you are purchasing is of equal or greater value than your existing property, which is currently used as security for your loan. The property should also be considered acceptable in terms of location, condition and marketability.

Get a buyer’s agent to help find suitable properties and negotiate favourable terms!

What if my current loan cannot cover the purchase of my new property?

If your current loan doesn’t cover the purchase of your new one or you are unable to afford the purchase. You can still proceed with loan portability, but you’ll need to apply for a loan increase first. Once it is approved, your portability loan can then be transferred to the new property.

What happens if I purchase my new property before selling the existing one?

If you purchase before selling, home loan portability is still possible, but not without a bridging loan. Here, a bridging loan allows you to purchase your new property before selling your existing one. Once your current property is sold, the bridging loan is closed, and your existing loan is transferred to the new property through loan portability.