When comparing home loan features, one of the most common questions borrowers ask is: offset account vs redraw, which is better?

Whether you’re applying for a new mortgage or looking to refinance your home loan, understanding offset and redraw can potentially save you thousands in interest and help you manage your money more effectively.

Both features are designed to reduce the interest you pay on your home loan, but they work in very different ways. Further, we’ll be helping you break down the functions, so you know exactly what to use for your upcoming home loan.

Read: How to Improve Your Credit Score? Tips to Fix Your Credit Report!

What is an Offset Account?

An offset account is a powerful home loan tool that combines everyday banking with an interest-saving feature. As a mortgage broker myself, this is how I see it: an offset account is essentially a regular transaction account, like your savings or checking account, but it’s linked directly to your mortgage.

Killing two birds with one stone, you can use it for everything from receiving your salary to paying bills, shopping or withdrawing cash, all while helping reduce the interest charged on your loan.

What makes an offset account unique is how it interacts with your loan balance. Instead of earning interest like a traditional savings account, the money sitting in your offset is used to reduce a portion of your home loan that is subject to interest. In simple terms, your lender calculates interest on your loan balance minus whatever is in your offset account.

Are you self-employed, looking to get a home loan? We have all the tips and tricks you need!

Let’s suppose you owe $500,000 on your home loan and have $50,000 in your offset account; you’ll only be charged interest on only $450,000. Which means you significantly reduce the total interest you pay over the life of the loan, especially if you maintain a healthy balance in the account over time. Try using our home loan offset calculator for accurate results based on the data you provided.

Your home loan interest is calculated daily and charged monthly, which means every dollar in your mortgage offset account is working for you every single day. Even short-term deposits can contribute to reducing your interest. Over several months and years, these small daily savings can add up to substantial long-term benefits.

Pros

- Reduces Interest: One of the biggest benefits of an offset account is its ability to reduce the amount of interest you pay on your home loan. Because the balance in your account is offset against your loan, you’re effectively lowering the portion of your loan that accrues interest. With time, this can lead to significant savings and even help pay off your home loan faster.

- Flexibility: Having an offset account means maximum flexibility. You can use your offset account just like a regular bank account, deposit your salary, pay bills, transfer funds or withdraw cash whenever needed. This sort of convenience makes it easy to integrate into your everyday financial routine.

- Easy Money Management: By combining your spending, saving and loan strategy all in one place, you can streamline your finances and make your money work more efficiently without needing multiple accounts.

- Tax Benefits: An offset account can be especially strategic for property investors, as it allows you to leave rental income or surplus funds in the account to reduce interest, without actually paying down the loan principal. This becomes especially beneficial from a tax perspective, as it keeps the original loan structure intact.

Cons

- High Fees and Charges: Many home loans that offer offset accounts come with higher interest rates or annual package fees. This means the savings you generate from the offset need to outweigh these additional costs for it to be worthwhile.

- Requires High Account Balance: Another limitation of offset accounts, especially for those who lack reasonable finances, is that it is only truly effective if you have and maintain a reasonable balance in it. If your account balance is consistently low, the interest savings may be minimal, which reduces the overall value of having the feature.

- Types of Offsets: You need to remember that not all offset accounts are created equal. Some lenders offer partial offset facilities rather than a full 100% offset, meaning only a portion of your balance reduces your loan interest. This can limit the potential savings.

- Financial Discipline Required: In the end, for you to minimise the access to your funds, you need a level of financial discipline. Because the money is readily available, it can be tempting to dip into it for everyday expenses or non-essential wants. If not managed carefully, the effectiveness of offset accounts can be reduced.

Find out how much you can borrow against the value of your property by calculating your loan to value ratio!

What is Redraw on a Home Loan?

A redraw facility is a feature built into the home loan that allows you to access any extra repayments made above your minimum required repayments. To explain simply, if you’ve been paying more than you need to on your mortgage, you may be able to redraw those additional funds later whenever you want.

This way, you will basically be getting ahead on your loan while still having that safety net. You can choose to make extra repayments regularly or as occasional lump sums. You are left open to decide how or when you wish to contribute. These additional payments go directly toward reducing your loan principal, which in turn lowers the amount of interest charged.

Refinance your home loan to get better rates and features!

Please note that redraw is only available on surplus payments. If you’ve only ever met the minimum required repayments, there won’t be any extra funds available to access. Redraw account builds its balance over time through consistent overpayments.

A redraw facility can have a few conditions around how much you can withdraw and how often you can access it, or how quickly the funds are released, all depending on your lender. It encourages you to reduce your debt first, while still offering a level of access to your extra repayments when you truly need it.

Fund your self-managed build with owner builder loans!

Pros

- Maintains Balance: A redraw facility offers a practical balance between reducing your home loan and maintaining access to your extra funds.

- Helps Lower Loan Principal: Any additional repayments you make go directly toward lowering your loan principal. With a redraw account, you are not just saving money, you’re actively reducing your debt while still retaining the option to access your extra funds whenever needed.

- A Cost-Effective Approach: In several cases, redraw facilities are either free or come with very minimal fees, making them a more affordable option compared to an offset account, which often comes with annual package fees or slightly higher interest rates.

- Builds Financial Discipline: Since accessing the funds isn’t as immediate and seamless as withdrawing from a regular bank account, borrowers are generally less tempted to dip into their extra repayments for everyday expenses.

Did you know that you could use your superannuation to buy a house?

Cons

- Difficulty Accessing Funds: Accessing money through a redraw may take time. Depending on your lender, there could be delays, minimum withdrawal amounts, or specific conditions that need to be met before you can access your funds.

- Impact on Tax Deductibility: Particularly for investors, if you redraw funds from a loan that is or will be used as an investment property, and then use that money for personal expenses such as a car or a holiday, it can complicate or reduce the portion of interest that is tax-deductible. Consider seeking professional financial advice before using redraw funds in situations like this.

- Restrictions on Facilities: Some lenders place restrictions on redraw facilities, such as limiting how often you can withdraw funds or capping the amount you can access at any given time. These limitations can reduce flexibility and make it harder to rely on redraw as a readily available financial cushion.

Try debt recycling to turn your home loan debt into tax deductible debt!

The Similarities: Offset Account Vs Redraw

Before diving deeper into the offset account vs redraw debate, it’s important to understand that both features are designed with the same core goal in mind, i.e., to help you reduce the cost of your home loan and become debt-free sooner.

Find out what happens on settlement day to reduce moving stress!

This is something I often explain to my clients: at a fundamental level, both offset accounts and redraw facilities work to minimise the amount of interest you pay. They do this by lowering the effective balance on which your loan interest is calculated. Whether it’s through holding money in an offset account or making extra repayments on your loan through a redraw facility, the result is the same: less interest over time!

Another similarity is their ability to help you pay off your home loan faster. By reducing the interest charged, more of your regular repayments go toward the principal rather than interest. Over the life of the loan, this can significantly shorten your loan term and help you save a substantial amount of money.

It’s worth noting that both these features are also commonly available on variable rate home loans, making them accessible to many borrowers. While the exact structure and availability can differ, they are widely offered as tools to give borrowers more control over their loans and financial strategy.

Ultimately, despite there being clear differences in how offset and redraw accounts operate, both options serve a similar purpose.

Difference Between Offset and Redraw

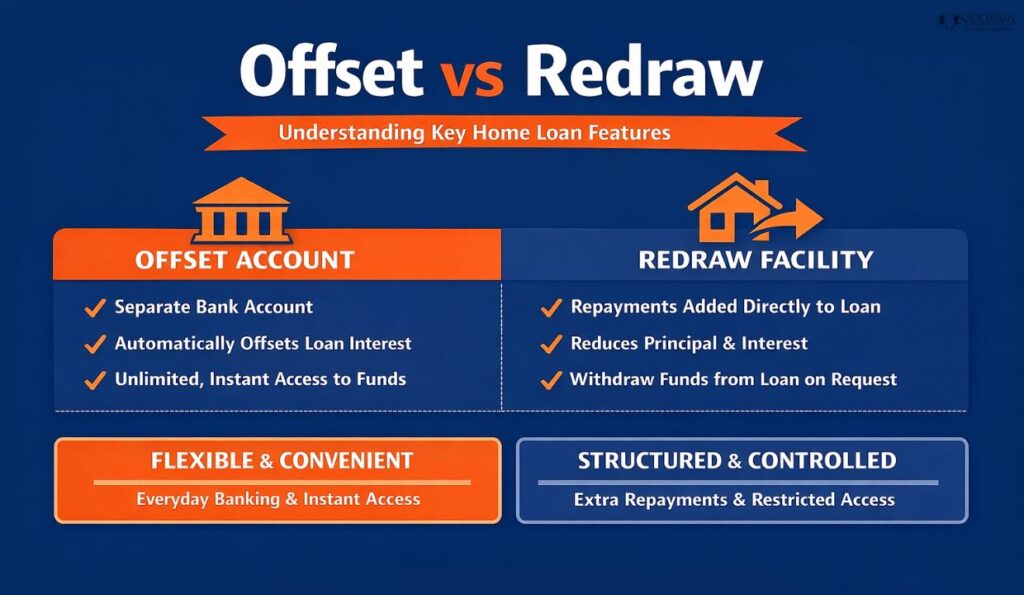

When one is comparing an offset account vs redraw facility, the key difference comes down to where your money sits and how accessible it is.

Where an offset account is a completely separate transaction account linked to your home loan, a redraw facility is built directly into your loan. With an offset account, your money remains in a bank account that you can control and use, while still reducing your loan interest. However, with redraw, your extra funds are paid into the loan itself as additional repayments, reducing your principal, but only accessible when you actively withdraw them.

You Might Be Interested In: Lenders Mortgage Insurance (LMI): Everything You Need to Know.

Another difference lies in how the balances are treated. Money in an offset account remains untouched by your loan repayments. It sits separately and continues to offset your interest regardless of your repayment schedule. Whereas redraw funds are created only when you make extra repayments on top of your minimum required amount. These extra payments directly reduce your loan balance.

Find out how salary sacrifice affects your home loan application!

When it comes to functionality, an offset account behaves just like an everyday bank account. You can have your salary paid into it, set up automatic bill payments, use a debit card, withdraw cash and manage daily expenses, all while reducing your interest. A redraw facility, on the other hand, is more limited. While you can access your extra repayments, it usually requires transferring funds out of your loan, and may be subject to conditions, limits or processing times depending on the lender.

Buy a new home before selling your current one with bridge loans!

Where redraw facilities are commonly included with many home loans, offset accounts are only offered with certain loan products, often those with higher fees and package structures.

How you grow your balance also differs between offset and redraw accounts. With redraw, you need to actively make extra repayments, either manually or via direct debit, to build up available funds. With an offset account, you can simply deposit your income, savings or surplus cash into the account and immediately start reducing your interest.

Try the Help to Buy Scheme and purchase a property with a much smaller deposit than traditionally required!

Finally, access and discipline play a huge role. A redraw facility tends to restrict access slightly, which can actually be beneficial if you’re trying to stay disciplined and save for a specific goal like renovations. An offset account, by contrast, offers unlimited and instant access to your money, giving you flexibility but also requiring more self-control to maintain a meaningful balance.

In short, the difference between redraw and offset comes down to flexibility versus structure. Where offset represents convenience, accessibility and everyday use, redraw facility represents structured repayments with controlled access to extra funds. Understanding what works best for you is key to home loan success.

Find out how much you need for a house deposit.

Who Can Benefit from an Offset Account?

Offset Accounts are best suited for borrowers who want a simple, all-in-one way to manage their everyday banking while also reducing their home loan interest. It works particularly well for people who like the convenience of keeping all their finances in one place.

Secure your home loan journey by asking important questions to your mortgage broker with zero hesitation!

This setup is useful for individuals or households who rely heavily on automated banking. If your income is regularly deposited into your account and your expenses, such as utilities and rent, are set up on a direct debit, an offset account can quietly work in the background to reduce the interest you pay without any extra effort.

Rent now with the option to purchase the same property later with Australian Rent to Buy Schemes!

If you are someone who tends to hold surplus cash, offset accounts can be an option for you, too. Even with smaller balances, sometimes offsets can prove beneficial. For example, if your lender offers multiple offset accounts at no additional cost, you may still benefit by spreading funds across different goals while collectively reducing your loan term.

In short, an offset account is best suited for disciplined borrowers who can maintain a consistent cash flow in the account while still managing everyday spending responsibly.

Calculate your rental yield to figure out your real profit after expenses on your investment property!

Who is a Redraw facility for?

A redraw facility is often best suited for owner-occupiers. For those who want a straightforward and cost-effective way to reduce their home loan without a separate banking structure, it’s the best option out there.

In many cases, redraw is included as a standard feature on home loans at no extra cost, making it an attractive option for borrowers who prefer simplicity and value for money.

Rent wherever you want while investing where you can afford by rentvesting to boost your overall capital growth!

If you don’t constantly have large cash balances to manage, a redraw facility can be more effective compared to offset accounts because it focuses on reducing your loan balance directly through extra repayments rather than relying on idle cash lying in your account.

If you can make extra repayments when possible, whether that’s small, regular contributions or occasional lump sums, a redraw facility can help these payments go directly into your home loan, reducing the principal and, in turn, the interest charged. Over time, you not only reduce the overall term of your loan but also build home equity faster.

To conclude, redraw is often a better fit for those who prioritise low costs, simplicity and structured debt reduction over the everyday flexibility of a transaction-based account.

Did you know there was a flexible home loan option for self-employed and non-traditional borrowers? Learn more about it with low doc home loans!

Is Offset or Redraw Better?

It might come as a shock, but there isn’t a clear winner in the offset account vs redraw debate. Both features have strong benefits, and the right choice depends on your personal financial situation, your spending habits and long-term goals. In fact, you should rather be asking, which one is the best for you and not which is inherently the best, because there isn’t one clear answer.

Offset accounts are not available on every loan product and are often linked to specific packages or variable rate loans with slightly higher fees or interest rates. Redraw facilities, on the other hand, are far more widely available and are usually included by default, as long as you make extra repayments above your minimum requirement.

Also Read: How Much House Can I Afford?

If you’re someone who can consistently pay more than the minimum repayment and occasionally set aside lump sums, a redraw facility may be a strong fit for you. It allows you to reduce your loan balance faster and pay less interest over time. While you can usually access those extra repayments when needed, doing so reduces the long-term interest savings benefit, so it works best when you can keep away from using the extra amount.

On the other hand, if you prefer easy access to your money and want the convenience of using a single account for everyday banking, an offset account may be more suitable. It not only offers instant access to funds but also continuously reduces the interest charged on your home loan.

Secure your dream property without an upfront deposit with a deposit bond!

Please note that there are important tax considerations, especially if you’re a property investor. For a property that is used as an investment that generates rental income, the interest on your loan may be tax-deductible. An offset generally does not affect this structure. However, with a redraw facility, withdrawing funds and using them for personal expenses can potentially impact tax deductibility, making it important to seek professional advice before making changes.

In the end, whether you choose an offset or redraw, it all comes down to how you manage your money. If you value flexibility and everyday access, Offset may suit you better. If you prefer structured savings and disciplined debt reduction, redraw could be the better option. Choose wisely!

Access several government grants and schemes as a first home buyer and maximise savings on your home loan!

Can I Use Both an Offset Account and a Redraw Facility?

Well, you don’t necessarily have to choose one over the other. Some lenders offer home loans that include both an offset account and a redraw facility, giving you the flexibility to benefit from everyday interest savings while still making extra repayments to reduce your loan faster. If you can handle the requirements, using both is totally possible.

Need Help?

If you’re still feeling unsure or going in circles trying to compare offset account vs redraw facility, it may be worth speaking with a trusted home loan specialist who can break it down for your situation. At Nice Loans, your trusted mortgage specialist, we help borrowers understand how each feature works in practice, not just in theory, so you can make a confident decision that actually suits your lifestyle.

We can compare lenders and explain which home loans offer offset accounts or redraw facilities. The goal is to match you with a structure that supports your financial goals, whether that’s paying off your home loan sooner, improving cash flow or maximising savings.