The Help to Buy scheme is an initiative introduced by the Australian government to help eligible home buyers purchase a property with a much smaller deposit than traditionally required. Under the scheme, the government contributes a portion of the property’s purchase price, becoming a co-owner alongside the buyer.

The shared ownership reduces the size of the mortgage required, making home ownership more achievable for low to middle-income Australians who have been locked out of the market due to rising house prices and home loan deposit requirements. The approach makes entering the property market less daunting and more achievable, particularly for young buyers, single parents, families and individuals re-entering the housing market after significant life changes.

The program proposed by the Australian Labour Party in 2022 to address housing affordability passed through parliament in late 2024. With applications having opened on 5 December 2025, eligible homebuyers can now lodge their appeals under the scheme.

Want a home loan with zero deposit? Read our piece on No Deposit Home Loans to learn more!

What is the Help to Buy Scheme?

The Help to Buy scheme, as the name suggests, assists eligible buyers in purchasing a home with a minimum deposit of just 2% by allowing the federal government to contribute up to 40% of the purchase price for a new home and up to 30% for an existing home.

In return, the government holds an equivalent equity stake in the property. Buyers are not required to pay rent or interest on the government’s share. Such a generous structure significantly reduces the size of the mortgage, monthly loan repayments and the need for Lenders Mortgage Insurance (LMI).

Save thousands on your mortgage interest by linking your transaction account to your home loan through offset accounts!

Unlike grants or guarantees, Help to Buy is a co-ownership model, meaning any future capital growth is shared proportionally with the government. The scheme aims to help 40,000 households over the span of four years; 10,000 each year is the ultimate target.

Try bridging finance if you find your dream home before you are ready to sell your current property. Move with your purchase without waiting for your existing home to sell!

How does the Government Help to Buy Scheme work?

Help to Buy is a shared equity scheme where the Australian government contributes towards the purchase of a home. It operates along with a standard home loan from a participating lender. Buyers must contribute a minimum 2% deposit of the property’s purchase price using genuine savings. This deposit is paid upfront at the time of purchase, demonstrating the buyer’s financial commitment to the property.

Given that the government contributes a differing percentage to the purchase price depending on whether the home is new or existing, the contribution reduces the size of the mortgage required accordingly. The government becomes a silent co-owner, with no involvement in day-to-day living decisions but with a considerable equity share in the property.

Negatively gear your investment property to achieve long-term capital growth and tax benefits!

The remaining portion of the purchase price is financed through the lender. Buyers must meet the lender’s usual prerequisites and credit requirements, although the reduced loan amount can make approval easier. Loan terms, interest rates and repayment structures are set by the lender and not by the government.

Buyers are not required to pay rent or interest on the government’s share of the property. This is a key difference from many private shared-equity arrangements and helps keep ongoing housing costs more affordable. Although ownership is shared, the buyer is fully responsible for mortgage repayments, council rates and utilities, property maintenance and repairs, building and contents insurance and other miscellaneous fees if applicable.

Purchase your dream property without an upfront deposit with Deposit Bonds!

Eligibility Criteria

To qualify for the government’s Help to Buy scheme, applicants must meet strict eligibility requirements. The Help to Buy eligibility criteria are listed below:

- Be an Australian Citizen.

- Be at least 18 years old.

- Meet the income caps.

- Has saved at least a 2% deposit.

- Live in the purchased property as their principal place of residence.

- Doesn’t currently own or have ownership interest in another property in or outside Australia.

- Be able to cover upfront costs. Everything, including stamp duty unless exempt, legal and conveyancing fees, bank and settlement fees.

The scheme is not limited to first home buyers and may also apply to individuals re-entering the property market following significant changes in their personal or financial circumstances.

Are you a single parent looking for alternatives to buy your first home? The Family Home Guarantee Scheme might be just the option for you.

What are the Property Price Caps on the Federal Government Help to Buy Scheme?

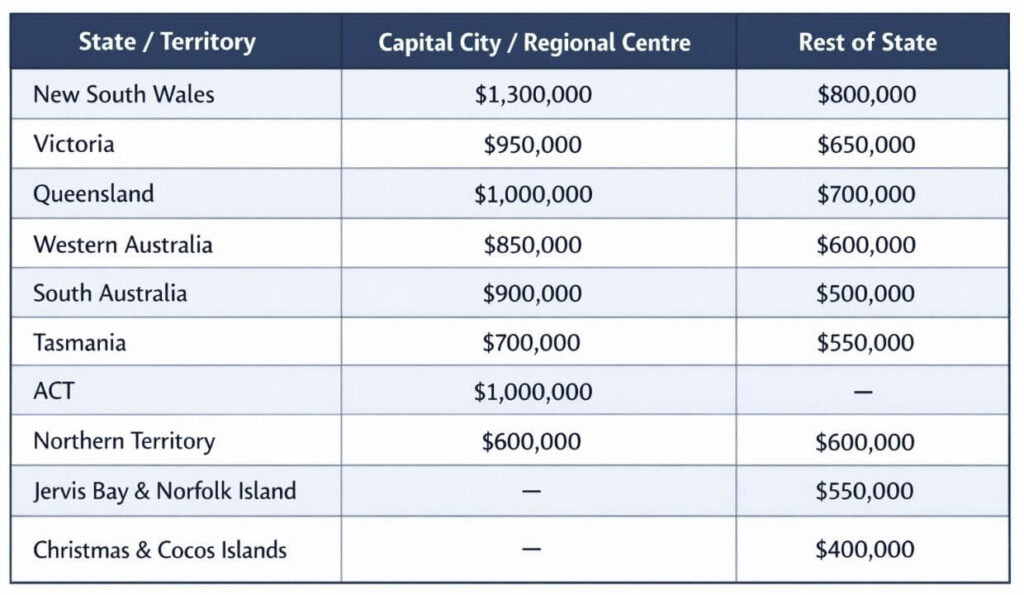

Property price caps on the Help to Buy scheme apply and vary by state and territory, reflecting local market conditions. With the focus being on low-income households, the caps ensure the scheme remains targeted at modestly priced homes rather than premium properties.

Please note that not all states and territories may have passed the enabling legislation to participate in the scheme. Make sure to consult with your lender about your location and if it’s currently included.

Ever tried to assess your financial capacity to own a home? Discover how much house you can afford on your budget!

What are the Property Caps?

Not all properties are funded by the Help to Buy Scheme. Provided that the properties fall within relevant price caps and meet the lending requirements, established or newly built homes, off-the-plan properties, apartments and units, townhouses and house and land packages are generally permitted. The property must be suitable for residential living and purchased as the buyer’s primary place of settlement. Investment properties and holiday homes do not apply.

Read: Refinancing a Home Loan with Bad Credit.

Application Process

Applying for the Australian Government Help to Buy Scheme involves key stages, from checking eligibility to settlement. While the process is similar to a standard home loan application, it also involves additional steps due to the government’s involvement in the shared equity initiative.

Check Eligibility: Before applying, confirm that you meet all eligibility requirements, including the income limits, the minimum 20% deposit requirement, property price caps for your state or territory and the usual proof of identity verification. At this stage, speaking with a mortgage broker can be particularly helpful. A broker can thoroughly assess your financial position, explain how the scheme works and identify participating lenders that suit your circumstances.

Apply Through a Participating Lender: Applications must be submitted through a participating lender, not directly to the government. The lender will assess your annual taxable income, expenses, credit history and borrowing capacity. It’s only after they confirm your ability to service the reduced loan amount that they’re confident enough to sign with you. They ensure that the property type you intend to purchase meets scheme rules. If you pass the lender’s assessment, they submit your application to Housing Australia for Help to Buy consideration.

Calculate the rental yield on your property to find out the amount of money you will make compared to its inherent value!

Pre-approval and Scheme Reservation: Once Housing Australia approves your application, your place in the Help to Buy scheme is reserved for 90 days. An extension may be requested if you are actively searching for a property and your circumstances have not changed. While a pre-approval isn’t a formal guarantee, much like a conditional loan approval compared to an unconditional approval, it still confirms your eligibility, your price and the state or territory your approval applies to.

Property Search: With pre-approval secured, you can begin searching for the appropriate property. Make sure that the home falls within your approved price limit, meets Help to Buy property eligibility and is located in the approved state or territory. Stay informed according to your pre-approval letter to have a clear guide during your property search, and provide it to real estate agents if required.

You might be interested in: How Do Rent to Buy Schemes Work?

Contract and Final Approval: Once you find a suitable property and agree on a purchase price. Your solicitor or conveyancer reviews the contract of sale, you sign the contract and pay the deposit. Your lender updates your application with the property details. The lender then submits the final application on your behalf to Housing Australia, which completes the final assessment and formally confirms your participation in the scheme.

Are you self-employed, looking for a home loan? Find out how to land the best loan rates even if you’re self-employed!

Settlement: Before settlement, you must arrange building insurance effective from the settlement day. Remember to provide proof of insurance to your lender and Housing Australia. On the day of the settlement, funds are transferred from the lender and the government and legal ownership is registered. With that, the mortgage and shared equity arrangements are finalised. The property is then officially your home, and you begin making repayments as required.

Check Out: What is a Low Doc Home Loan?

Help to Buy Scheme for First Home Buyers vs Returning Buyers

Unlike several ownership initiatives, the Help to Buy scheme is not limited to first-home buyers; individuals or couples who previously owned a property but are re-entering the market due to major life changes are also eligible. In both cases, the scheme helps buyers reduce the size of their mortgage, lower repayments and cancel out the LMI.

As a returning buyer, you could’ve gone through a major financial hardship, a divorce or separation or are looking to either downsize or upsize. In such cases, you can take advantage of a low deposit entry even if you no longer have property ownership. The shared equity scheme makes housing more affordable, especially in highly priced areas.

Eligible first home buyers also benefit substantially from the scheme. They can enter the market earlier, avoid LMI and combine Help to Buy with other First Home Owner Grants and Schemes, depending on their state or territory. Such buyers often gain the largest advantage because the scheme is much easier on their budget compared to applying for a traditional loan.

Help to Buy Scheme Pros and Cons

Every policy comes with both advantages and trade-offs, and the Help to Buy scheme is no exception. It can be a valuable pathway into home ownership for eligible buyers, but it is not suitable for everyone. Understanding both the benefits and limitations is essential before making any sort of commitment.

Also Read: Understanding Debt to Income Ratio in Australia.

Pros

- Quicker Access to the Property Market with a Very Small Deposit: One of the biggest advantages of the Help to Buy scheme is the ability to buy a home with a deposit as low as 2 per cent. This dramatically shortens the time needed to save and allows buyers to enter the market years earlier than previously expected.

- Lower Mortgage Repayments: With the government contributing up to 30% for existing homes and 40% for new homes, buyers need to borrow significantly less. A smaller loan means lower monthly repayments, improving cash flow and reducing financial stress.

- No Lenders Mortgage Insurance (LMI): A higher combined equity position due to government contribution, buyers generally avoid paying Lenders Mortgage Insurance (LMI), which saves them tens of thousands of dollars upfront or over the life of the loan.

- Ability to Buy the Government’s share over time: Participants can gradually increase their ownership by buying back all or part of the government’s equity when their financial situation allows. This flexibility is a big motivator for buyers to work toward full ownership on their own pace.

- Targeted Assistance for Lower-Income Households: Strict income and property caps ensure the scheme is focused on low to middle-income Australians who have been pushed out of the market, rather than investors or individuals with high incomes.

Cons

- Shared Capital Gains with the Government: With the government owning a portion of the property, any capital gains are shared when the property is sold or when equity is bought back. If the property price increases significantly, buying out the government’s share may become more expensive over time.

- Restrictions on Selling or Refinancing: Selling the property or refinancing your home loan or making certain changes to the property often requires approval from Housing Australia. These conditions can reduce flexibility compared to owning a home outright or through normal loan processing.

- Potential Requirement to Buy Out Government’s Equity Share: If a participant’s income exceeds the scheme’s income cap for two consecutive years, they may be required to start buying back the government’s share. This can create financial pressure if income rises faster than expected, but the expenses still cause stress.

- Limited number of places available: The Help to Buy scheme is capped, with a fixed number of places available nationally every year. Demand may exceed supply, meaning even if you’re eligible, you might not secure a place. This can be absolutely discouraging.

Help to Buy Scheme QLD

Queensland applicants are eligible for the Help to Buy Scheme under the national framework, with conditions tailored to reflect local property markets. As with all states and territories, Queensland buyers must meet the scheme’s income limits, deposit requirements and owner-occupier rules.

Capital city and major regional centres are subject to a higher price cap of up to $1,000,000. This includes Brisbane and designated regional centres such as the Gold Coast and the Sunshine Coast. All other areas of Queensland are subject to a lower price cap of up to $700,000.

Also Check Out: Can I Use My Super to Buy a House?

Remember that the buyers still ought to comply with Queensland stamp duty rules; in case you have qualified for any concessions or incentives, exemptions are possible. Buyers are also responsible for upfront costs, including legal fees, inspections and lender charges.

The Help to Buy scheme is a golden opportunity for Australians who have long dreamed of owning their own home but have been held back by high deposit requirements and unaffordable monthly repayments. With limited places available, securing your spot is essential. Get in touch with Nice Loans, your trusted mortgage broker based in Brisbane, to learn more and discover exactly how the scheme can work for you.

FAQs

When will the Help to Buy scheme start?

The Help to Buy scheme commenced on 5 December 2025, when applications opened nationwide. Eligible Australians can now apply for the scheme through participating lenders. Early preparation and securing pre-approval are strongly recommended.

How many homes is the Help to Buy scheme willing to fund?

The Australian Help to Buy scheme is set to fund a total of 40,000 homes over a period of four years, with 10,000 places made available each year.

Can I increase my stake in the property?

Yes. Participants can increase their share of the property by buying back part or all of the government’s equity over time. The process can be long and usually done in stages rather than all at once.

Go for debt recycling to build wealth while paying off your home loan faster than ever!

What if my income increases?

If your household income rises above the scheme’s income threshold for two consecutive years, you may be required to start buying back the government’s equity. An income increase does not immediately remove you from the scheme, but the policy ensures that their initiative stays for those who need it the most.

Can I renovate my Home?

Yes. Minor renovations are not a problem, but major renovations or structural changes require prior approval from Housing Australia. This is because renovations can affect the value of the property, thus the government’s equity.

Can I sell the property?

Yes. You can sell your home whenever you like; however, with standard selling requirements in mind. When the property is sold, the proceeds are distributed according to the ownership shares held at the time of sale.

Can the Help to Buy Scheme be combined with other government initiatives?

The Help to Buy scheme can often be used alongside other government initiatives. Since eligibility depends on the rules of each program, it’s best to consult and confirm compatibility with your lender or mortgage broker before proceeding

Who are the participating lenders that I can apply through?

Not all banks or lenders are part of the Help to Buy scheme just yet. Currently, you can apply through two main lenders, Commonwealth Bank (CBA) and Bank Australia.