Why do you think it’s necessary to understand how to get pre approved for a house loan? It’s not even unconditional approval we’re speaking of, so why the emphasis? To understand, we have to take it from the beginning.

One of the biggest challenges many buyers face when looking to buy a home is understanding their financial capacity. For most people, the main concern is whether they can afford the property they want to build or purchase.

Without a clear understanding of how much you can borrow, it can be difficult to confidently attend property inspections, participate in auctions or submit offers on homes that pique interest. You may likely end up spending time looking at properties that are outside your budget or missing essential opportunities just because you’re unsure about financing. This is exactly where home loan pre-approval comes in play.

Rent now with the option to buy later with Australian Rent to Buy Schemes!

A pre-approval gives you a clearer idea of your price range before you begin house hunting seriously. With that, you can focus on property searches that match your budget, making the process more efficient and less stressful.

While it is true that pre-approval does not guarantee final loan approval, it provides valuable guidance and confidence as you begin exploring the property market.

Do you want to pay off your mortgage fast? Here are all the tips you need to be mortgage-free in only 10 years!

What is Home Loan Pre Approval?

A home loan pre approval, also known as conditional approval, is when a lender indicates that they are willing to lend you a certain amount for a home loan, provided specific conditions are met.

Not only does it provide an estimate of how much you may be able to borrow, but it also gives you an assessment of your financial situation that becomes the groundwork for future unconditional home loan approval or full approval.

Build your own home with owner builder construction loans! Learn how to get approved for a construction loan, now!

You will have noticed the mention of two typical stages of approval in the home loan process:

- Conditional Approval: An early stage of the process, which is useful when you are preparing to buy a property.

- Unconditional Approval: A Full Approval is what occurs later in the home loan process, usually after you have chosen a property and the lender has completed all necessary checks.

For a pre-approval, you can fill out an online application that takes around 30 minutes to complete, and depending on the information provided, you get your borrowing capacity estimate in no time.

Please remember that you may be asked to verify the financial information provided in the initial application. A request for conditional approval will typically be recorded on your credit history, regardless of the outcome, so going into it with care is essential.

Try debt recycling to turn your home loan debt into tax deductible debt!

Types of Pre Approval

To get pre-approved for a house loan, you must understand the types of preapprovals you can qualify for. Lenders typically offer two main types of pre-approval: system-generated pre-approvals and fully assessed pre-approvals. Understanding the difference between the two can help you choose the option that best suits your financial situation.

Buy a new home before selling your current one with bridging loans!

System Generated Pre Approvals

As the name suggests, system-generated pre-approvals are based on automated assessments that are the quickest and easiest to obtain. Using the financial information you provide through an online application, the system generates an estimated borrowing limit within a short period.

Given the swift exchange, it generally involves minimal verification of your financial details, which is why the estimate may not fully reflect your complete financial situation and may change once your documents are manually and formally reviewed by the lender.

However, system-generated preapprovals can be useful throughout initial planning. With a rough estimate, you can begin your property search at least.

Calculate your rental yield to find out your rental income compared to your property value!

Fully Assessed Pre Approvals

Fully assessed home loan pre approvals involve a more detailed assessment of your finances by the lender. During this process, the lender verifies supporting documents such as pay slips, bank statements, tax returns and other financial records.

This type of pre-approval delivers a more accurate and reliable representation of your borrowing capacity because of the thorough assessment involved. It considers important factors such as your income, ongoing expenses, assets, liabilities and credit history.

Ultimately, fully assessed pre-approvals are generally considered stronger and more dependable, particularly when you are ready to make your bids on property or participate in auctions. They provide both you and the sellers with confidence that the financing is likely to proceed smoothly.

It’s the best time to be self-employed! With low doc home loans, buy your dream home without the hassle of the usual loan requirements!

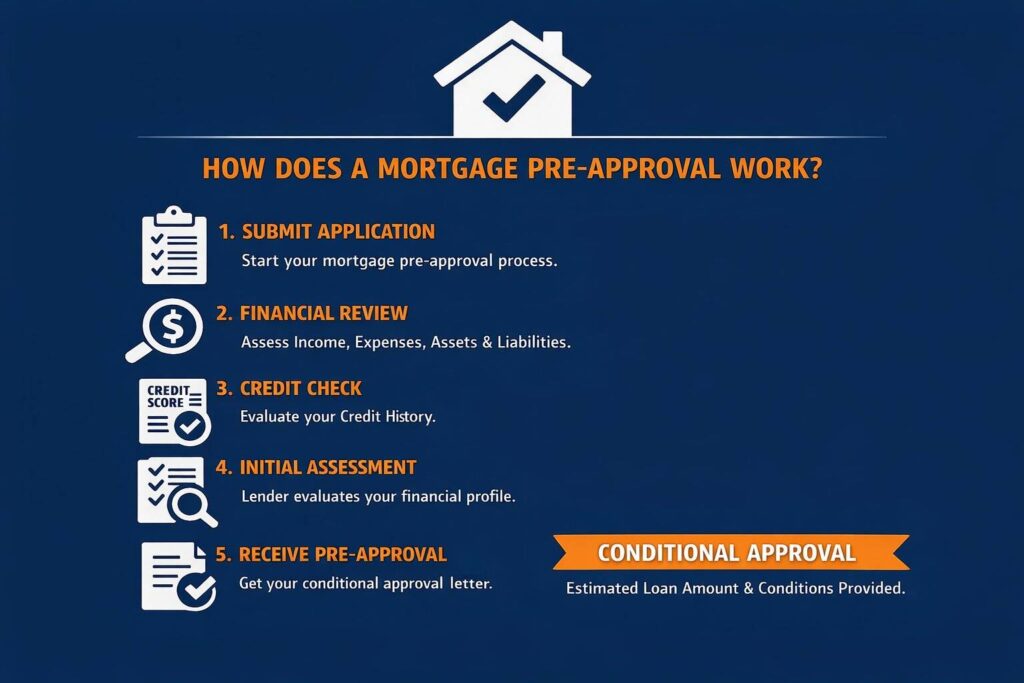

How Does a Mortgage Pre Approval Work?

Your lodged application for a mortgage pre-approval kickstarts the beginning of your home loan journey. First of all, the lender conducts a preliminary assessment of your financial position to determine whether you are even likely to qualify for the offered amount. Whether you get a home loan or not depends largely on your financial health. This process is vital, as it helps lenders evaluate your financial ability and, therefore, your borrowing capacity to determine the amount they may be willing to lend.

Read: Lenders Mortgage Insurance (LMI): Everything You Need to Know

As part of the assessment criteria, the lender will verify key aspects of your financial profile, including your identity, income and expenses, assets and liabilities. As proof, relevant documentation will also be required.

- Verification of Income and Expenses: Confirming your income sources and regular expenses helps lenders ensure that you have a stable financial situation and sufficient cash flow. You may be required to provide your payslips, utility bills to prove expenses, insurance, bank statements, etc.

- Assessment of Assets and Liabilities: Lenders will require documentation outlining your assets and liabilities. Assets may include your savings accounts, superannuation or other retirement funds, shares and investment properties. Liabilities represent existing debts and financial obligations, such as your credit card balances, personal loans or car loans. With this, the lender can assess your net financial position and debt obligation.

- Credit History Evaluation: Another essential component of the pre-approval process is a credit check. During this stage, the lender reviews your credit history to understand your borrowing behaviour and repayment patterns.

The overall review of your financial standing helps determine your reliability as a borrower. If the lender concludes after a thorough search that you meet their lending criteria, they will issue a written pre-approval, aka a conditional approval. This document outlines the estimated loan amount you may be able to borrow, along with any conditions that must be satisfied before final approval can be granted.

Looking to invest in properties? Understand the difference between negative gearing and positive gearing to make informed decisions throughout!

When to Apply for a Home Loan Pre Approval?

While it might not seem like much, timing plays a crucial role in the home-buying process. A pre-approval application lodged at the right stage can make your property search smoother, more efficient and less stressful. Prepping ahead and choosing that perfect moment to apply can help you navigate the property market with confidence and command.

Before you submit your pre-approval application, you need to make sure you have thoroughly studied the property market. Look into homes in areas that interest you and familiarise yourself with the typical price range. This initial research will help you avoid future disappointments. Realistic expectations allow you to narrow down your search and focus on properties that are within your budget.

Use online mortgage calculators and estimate your potential borrowing capacity beforehand. Even rough estimates can be helpful at the starting point! Another important factor is ensuring that your financial situation is stable. Review your finances and work on improving your credit report.

For better interest rates and loan terms, refinance your home loan!

Once all the prep is done, your house hunting is what influences when you apply the most. Generally, mortgage preapprovals remain valid for 60 to 90 days. However, this can vary between lenders. The limited validity period suggests that it’s best to apply when you are ready to actively start inspecting properties and making offers. Applying too early may result in your pre-approval expiring before you find the right home.

While the final stage, also known as unconditional approval, may require additional documentation and detailed checks, securing pre-approval allows you to begin with a clear financial roadmap.

Did you know that you could secure a property without an upfront deposit? Try deposit bonds to keep your funds in assets while still being able to purchase that dream property!

What Documents Do You Need to get Pre-Approved for a Home Loan?

Several documents are required to apply for home loan pre-approval. These documents help verify your identity, income, assets, debts and overall ability to manage loan repayments. The exact documents needed can vary depending on your circumstances, but the overall need for financial verification is homogenous. Here’s a comprehensive list to help you prep:

Buy that dream home with Nice Builds, your trusted home building partner!

Proof of Identity

Identity verification is crucial to lenders. This typically involves providing valid identification documents, including anything from a passport, driver’s license, birth certificate, or a medicare card, in certain cases. These documents confirm your identity and ensure the lender meets legal and regulatory requirements.

Access home equity without selling through home equity release and reverse mortgage options!

Proof of Income

To make sure that you’re able to repay the home loan, lenders require evidence of your income.

The documents required include:

- Payslips

- Bank statement

- Tax returns or notices of assessment

- A letter of employment from your employer

Understand the concept of loan to value ratio to find out how it impacts LMI payments!

In case you’re self-employed, you may be required to provide business statements, tax returns from previous years or an accountant’s letter before confirming your income. At the same time, if you receive income from other sources, such as bonuses, commissions, rental income or investments, you may need to provide documentation to verify these earnings.

Also Read: Refinancing a Home Loan with Bad Credit

Proof of Assets

Your assets give a clear view of your overall financial position and savings capacity. They may include:

- Savings Account

- Superannuation or other retirement funds

- Shares or other investments

- Vehicles owned

- Investment properties, if any.

The evidence of your assets helps demonstrate your financial stability and may strengthen your loan application.

The Australian Government Help to Buy Scheme helps you purchase a home with just 2% deposit!

Proof of Liabilities

Lenders also require information on any existing debts or financial obligations you may have. With this, they can calculate your debt to income ratio and determine exactly how much more debt you can reasonably manage.

Liabilities can range from credit card balances and limits to car loans, personal loans or student loans, if any. All outstanding debts also fall under liabilities.

Evidence of Living Expenses

Last but not least, lenders review your living expenses to understand your day-to-day spending habits. Why is it important? You may ask. It’s because your spending habits determine whether you can comfortably afford mortgage repayments.

Required documents may include:

- Grocery and household spending

- Utility bills

- Transport costs

- Insurance payments

- Internet and phone expenses

- Recreation and other miscellaneous expenses

Check Out: How to Get a Home Loan If You’re Self Employed?

By reviewing all of the above-mentioned documents. Lenders can form a comprehensive picture of your financial well-being and determine your qualification. To speed your overall approval, make sure to prepare these documents well in advance.

Find a guarantor for your home loan to purchase your property with a minimal deposit!

Does Pre-Approval Guarantee a Home Loan?

No, pre-approval does not guarantee an automatic home loan approval. At first glance, this may even seem unnecessary. If pre-approval doesn’t guarantee a loan, why is it considered at all?

The essential point here is that while it may not guarantee a full approval, it does help you get one. A pre-approval indicates that, based on the financial information you have provided, the lender is likely willing to lend you a certain amount. However, this particular assessment is conditional and subject to further verification later in the process.

In other words, pre-approval provides an estimate of your borrowing capacity but does not represent the lender’s final commitment to issue the loan.

Are you a single parent struggling to purchase your dream home? The Family Home Guarantee Scheme allows eligible guardians to buy with only 2% deposit and no LMI.

Why is Pre Approval Still Valuable?

Despite there being no guarantee of final approval, it remains valuable in the home-buying process. It provides a clearer understanding of your potential and helps you set a realistic budget while demonstrating your seriousness as a buyer.

Unconditional approval can be the final stage, but pre-approval ensures that you begin your home-buying journey with great clarity and preparation.

With no deposit home loans, buy your dream home with zero deposit!

What Happens After I am Granted a Pre Approval?

Once you receive your approval in principle, aka pre-approval, you can finally begin your property search. With a clearer and more realistic understanding of your budget, house hunting becomes much easier.

When you finally find a property that suits your needs, you can move forward with the formal home loan application process. At this stage, the lender will begin completing the final checks required before issuing unconditional loan approval.

The first step of the final assessment is typically a property valuation arranged by the lender. This valuation is conducted to ensure that the property’s market value supports the amount the borrower intends to borrow. In any case, if the valuation is lower than the purchase price, the final loan amount is affected, which can mean that you need a larger house deposit.

Next, you may need to arrange property insurance. This step needs to be taken care of before the loan is finalised. Alongside this, you need to proceed with finalising the contract of sale, which legally confirms the purchase of the property.

Please note that before granting final approval, the lender will also verify that your financial circumstances have not changed since the pre-approval was issued. Also, depending on your circumstances, you may need to fill out stamp duty concession or exemption forms, or apply for First Home Owner Grants and schemes if eligible.

Ultimately, with all conditions met, the lender will issue an unconditional approval, allowing the home loan to proceed toward settlement.

What If You are Denied a Mortgage Pre Approval?

Being denied a mortgage pre-approval can be disappointing, but it’s even more of a reason to prep better. In several cases, a pre-approval decline simply highlights areas of your financial profile that may need improvement, and it is perfectly doable!

- Find out why you were denied: Your lender or mortgage broker should be able to explain the factors that influenced the decision.

- If the denial is related to your credit score or existing steps, make an effort to strengthen your financial position.

- Lending criteria can vary between financial institutions. Just because one declined, doesn’t mean the other will too. Reach out to multiple lenders.

- A bank or financial institution that understands your financial history and has an established relationship with you can be more willing to work with you on a pre-approval solution. Consider speaking to them!

- Seek Help: An experienced mortgage broker or home loan specialist can review your financial situation, identify potential issues, and connect you with lenders that are more likely to suit your circumstances.

Looking for personalised assistance? Nice Builds is exactly what you need for a comprehensive review of your options! As a trusted mortgage broker based in Brisbane, our team is ready to guide you through every step of your home loan journey. Get in touch, now!

FAQs

How long to get pre approved for a mortgage?

Mortgage pre-approval can take anywhere from one to three business days, and depending on your lender and the complexity of your finances, the approval timeline can differ. Some lenders even make an offer on the same-day or provide instantaneous online pre-approvals, particularly when the application is system-generated.

Does applying for a pre-approval affect my credit?

Applying for a pre-approval does not directly affect your credit score. However, when you request a conditional approval, the lender conducts a credit check, and this inquiry is typically recorded on your credit report.

How long is the pre-approval valid for?

Most pre-approval letters remain valid for 60 to 90 days, although some lenders may extend the validity period up to 120 days. The duration can depend on several factors, including lender policies, your financial documentation, credit history and overall complexity of your finances.

Is getting pre-approved for a home loan mandatory when applying for a home loan?

No, a pre-approval is not mandatory when applying for a home loan. However, it is highly recommended for future buyers. Since it helps understand how much you may be able to borrow, its great help for those who want to focus on properties that match their budget without wasting time.

Can I get pre-approval for a mortgage if I’m a first-time home buyer?

Yes, first-time home buyers can absolutely apply for a mortgage pre-approval. In fact, it is often recommended before starting a serious property search.

Does getting a pre approval mean that I have to proceed with the home loan?

No, getting a mortgage pre-approval does not obligate you to proceed with the home loan. It simply suggests that a lender has reviewed your finances and indicated how much they might be willing to lend you.

Do you need to pay to get pre approved for a house loan?

No, you don’t, preapprovals are generally free of any fees and charges.

Figure out exactly how much house you can afford to begin budgeting for your dream property!