The Reserve Bank cash rate decision on September 30 is not the only big news for businesses right now – we’re also seeing costs shifting, confidence lifting and the ATO issuing guidance around company cars.

- Company car crackdown: what the ATO wants you to know

- Inflation rebounds to 2.8%, and may keep rising

- Business turnover surges in July

- ATO warns sole traders about common tax traps

Read more below.

Giving staff extra perks can be a great way to reward loyalty – but some perks can come with a sting in the tail. One common example is letting an employee use a work vehicle for personal trips.

The Australian Taxation Office (ATO) has warned that this can count as a fringe benefit and may trigger fringe benefits tax (FBT). That means your business could be hit with an unexpected tax bill, even if the vehicle isn’t used much outside work.

Personal use covers more than many people realise. It includes things like weekend camping trips, school runs, grocery shopping or driving friends and family around, according to the ATO. Even simply parking the car at an employee’s home overnight can be considered private use.

Some vehicles may be exempt from FBT if private use is minimal and the vehicle meets certain criteria. To stay compliant, the ATO recommends checking if exemptions apply, keeping accurate records such as logbooks and odometer readings, calculating your FBT liability, lodging and paying on time, and reporting any benefits on your employees’ income statements.

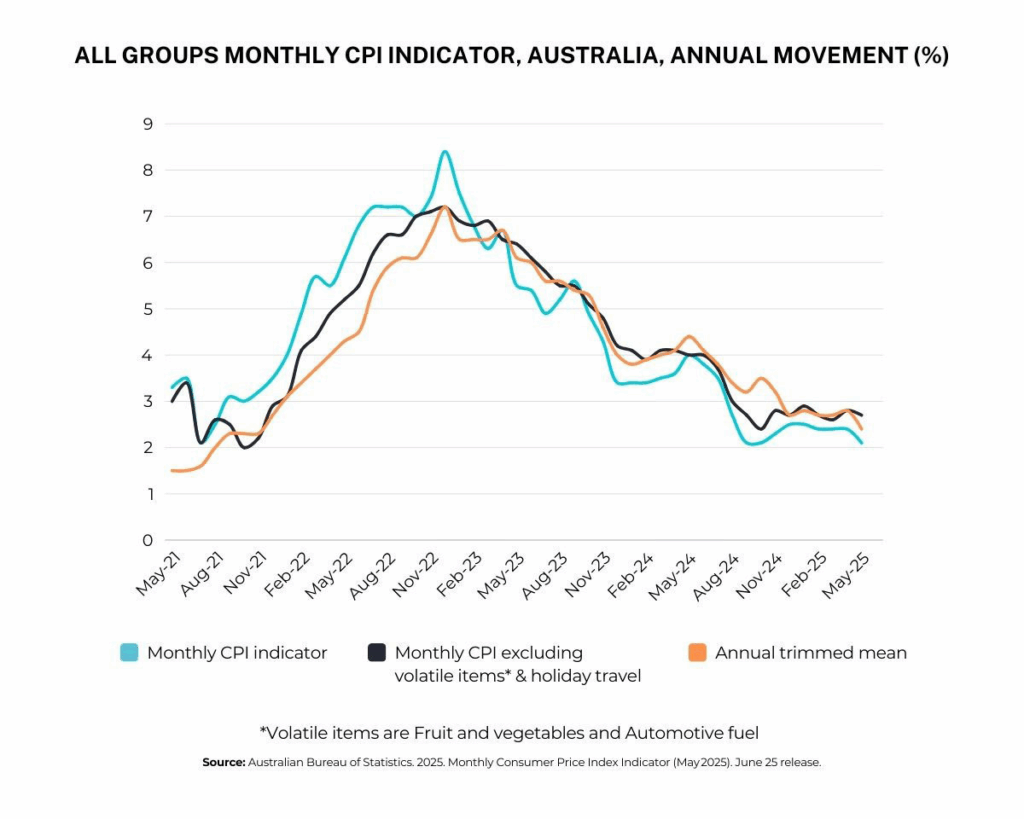

After easing for months, inflation has unexpectedly jumped – which could spell trouble for businesses trying to keep costs under control.

The Australian Bureau of Statistics reported that the consumer price index rose from 1.9% in June to 2.8% in July, pushing inflation back to the top of the Reserve Bank of Australia’s (RBA) target range. Earlier in the year, inflation had been trending down, giving hope of further interest rate cuts in the near future.

But those hopes may now be on hold. Annual inflation could climb even higher in the months ahead because prices actually fell in August and October last year – if those drops are replaced by price rises in the same months this year, the annual inflation figure will automatically rise.

Higher inflation makes it harder for the RBA to lower interest rates, which could keep loan repayments higher for longer. That means keeping an eye on your costs and finance arrangements is more important than ever.

Thinking about refinancing? Get in touch

After years of challenges, there are early signs of renewed momentum in the small business sector – with revenue climbing and confidence slowly returning.

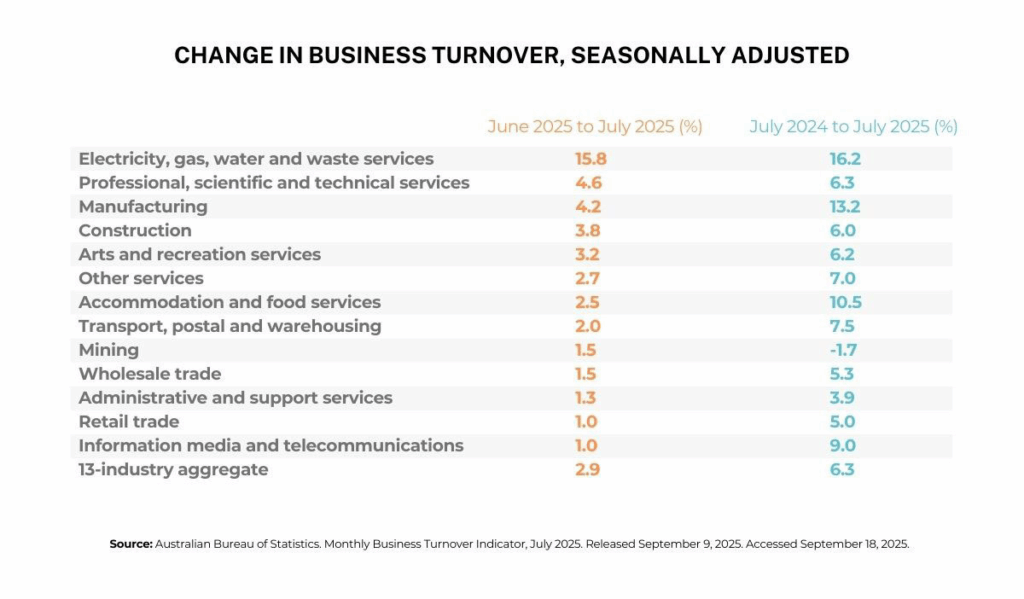

Business turnover surged 2.9% in July – the largest monthly increase in more than three years – taking annual revenue growth to 6.3%, according to the Australian Bureau of Statistics. All 13 industries grew month-on-month, and all but mining grew year-on-year.

Confidence is also improving. The Small Business Pulse, an index from the office of the small business ombudsman, Bruce Billson, rose 0.6% in August – the second consecutive quarterly increase.

Mr Billson said this reflected cautious optimism, with more business owners looking at ways to grow. He noted rising interest in using technology to boost productivity, streamline admin and reach customers through e-commerce, social media marketing and even artificial intelligence. Many are also reviewing suppliers, utilities and freight options to cut costs, while researching finance solutions such as invoice factoring to strengthen cash flow, he said.

Reach out to discuss your finance needs

Tax time can be stressful for sole traders – and small mistakes can lead to lost time and even unexpected tax bills. That’s why the Australian Taxation Office (ATO) has urged sole traders to double-check their returns and avoid common errors.

According to the ATO, some of the most frequent mistakes made by sole traders include:

- Not reporting all income – this can include side hustles, cash jobs or payments in-kind such as goods or services received in exchange for your work

- Over-claiming expenses – for example, claiming the personal portion of a cost or overstating business expenses

- Incorrectly claiming business losses – including offsetting non-commercial business losses against other income sources

- Misreporting personal services income – this can be done to gain tax benefits

- Failing to register for GST – if you are in the taxi or ride-sourcing industry, or if you meet the GST threshold

- Not keeping complete and accurate records

“We know small businesses work hard to get their tax and super right, however we understand mistakes can still happen,” the ATO said. “If you’re a sole trader, you can get ahead this tax time by avoiding these common errors.”