When applying for a home loan, especially as a first-timer, you’ll come across several unfamiliar terms, ones that are bound to leave you confused. Among them, two of the most important are conditional approval and unconditional approval.

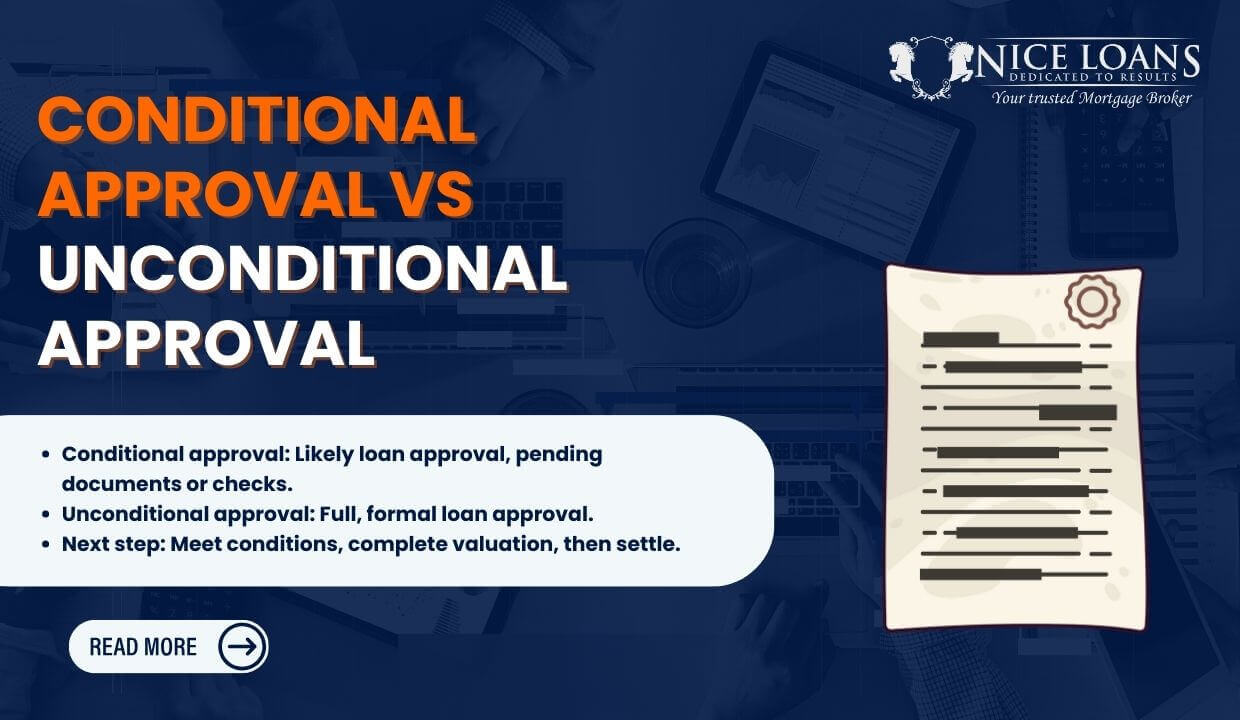

A conditional approval is an early stage in the home loan application process, and what you receive on your way to obtaining an unconditional acceptance. When you first apply for a home loan, you’re essentially applying for pre-approval. You submit your financial documents, such as payslips, bank statements and details of your assets and liabilities, so the lender can assess your economic position. If the lender is comfortable with your situation but still needs additional checks or documents, they issue a conditional approval.

You only receive unconditional approval once you’ve found a property, signed the contract of sale, usually with a finance clause, completed the valuation and provided all remaining documents requested by the lender.

You might be interested in: When to Refinance a Home Loan?

Difference Between Conditional Approval and Unconditional Approval

The key difference between conditional and unconditional approval lies in whether your loan can be fully approved or if it’s already been. Conditional approval indicates that a lender is willing to approve your loan, provided you meet certain requirements. Unconditional approval, on the other hand, means the lender is completely satisfied with your application. All checks and requirements have been met, and no further clarity is required; your loan is fully approved.

Conditional approvals help potential buyers understand their borrowing capacity, and are often helpful guides when it comes to house hunting. With unconditional approvals, you can confidently proceed with the property purchase, knowing that the lender is committed to providing the funds.

Don’t have a deposit saved for your dream home? There’s no need to worry, a no deposit home loan allows you to borrow the entire purchase price of your home without any upfront cost!

What Does It Mean to Be Conditionally Approved?

A conditional approval, sometimes also called pre-approval, is the first stage of entering into a loan contract. Think of it like Formula 1. Imagine you take pole position during qualifying, beating even Lando Norris, the season’s standout driver. Starting first on race day puts you at a strong advantage, but it doesn’t guarantee a win. You still need to perform on the main day, avoid mistakes and meet all the terms and conditions to take home the trophy.

Fund your self-build with owner builder home loans!

That’s exactly how conditional approval works; it puts you in a great starting position, but you must still meet the lender’s conditions before securing the final victory, your unconditional approval.

A conditional approval only enhances your likelihood of approval; provided that the lender’s requirements are met, the loan will be in your hands. It generally occurs during the mortgage underwriting process, when a critical evaluation determines whether the borrower is financially fit to undertake a large loan.

Read: Who can be a Guarantor on a Home Loan?

What does Unconditional Approval mean?

An unconditional approval, also known as formal approval, is issued when a home loan is fully approved by the lender. At this stage, your application is no longer subject to any conditions, and the lender who has confirmed all required checks and assessments is completely satisfied with your appeal.

Everything, including your financial situation, home loan deposit amount, loan to value ratio (LVR), property value and your ability to repay, is as required. Once unconditional approval is granted, you can move forward to signing loan documents, prepare for settlement and ultimately take ownership of your new home.

Are you a single parent looking to buy your first home? The Family Home Guarantee Scheme is just what you need, with a deposit as low as 2%, get a government guarantee backing you for a successful home loan approval.

What is Approval in Principle (AIP)?

Approval in Principle (AIP) is the first step with a lender in the home loan pre-approval process. The AIP indicates the amount you can borrow before finalising the property purchase. Based on your financial circumstances, the lender has an allocated amount they’re willing to lend you, and the AIP verifies just that. While it is no guarantee, it provides homeowners a sense of ease and confidence that the possibility of an approval for a home loan is not too far away.

Struggling with bad credit but still wish to refinance? Read our article on refinancing a home loan with bad credit for the best tips and tricks.

As with conditional vs unconditional home loan approval, the lender performs a preliminary assessment of your financial circumstances, given that a finance approval entirely depends on your income, expenses, credit history, loan repayments and other personal loans and monetary behaviour. An approval in principle is a form of conditional loan approval and doesn’t mean you’re fully approved; however, it is an essential part of getting an unconditional offer to speed up the approval process.

Borrow money using your home equity through a reverse mortgage!

What Happens After Unconditional Loan Approval?

Once you receive an unconditional loan approval, your home loan approval is absolute, and you can confidently move toward finalising your property purchase. At this stage, you can decide on how the property will be owned, whether you’ll be taking over as a sole owner or with a co-borrower.

Check Out: Can I Use My Super to Buy a House?

Within a week of approval, your lender will issue the loan offer documents. Remember to review all records carefully, check for errors or inaccuracies and seek guidance from your mortgage broker before signing and returning the documents. Do not deal with approvals in haste; returning documents promptly does help avoid delays, but a job done carelessly can lead to loss.

Building or home insurance has to take effect from the settlement date. The type of insurance you need may vary depending on your purchase, so have your mortgage broker or insurance agent help you choose the right policy. You may also be eligible for government grants and concessions, especially as a first-home buyer. The First Home Owner Grant (FHOG) or stamp duty concessions are a steal. These can provide significant savings, so it’s definitely worth exploring.

Pay the lenders mortgage insurance (LMI) premium and secure a home loan without a hefty deposit!

How Does One Get Conditionally Approved?

A conditional approval occurs when a lender needs additional confirmation before granting full, unconditional approval. The most common reason can be an error in your application. Your appeal may be missing key documents that loan underwriters need to verify your asset, debt and income information.

If your lender has been hesitant about passing your application, the issue is likely the verification you’ve provided. Perhaps you’ve missed something on your bank or asset statements? Or your loan or existing debt information is inaccurate? Underwriters require confirmation of all debts to calculate your borrowing capacity precisely.

Property investment doesn’t crumble at a few losses. Negatively gear your investment to achieve long-term goals and claim tax benefits, all thanks to the initial loss!

Apart from misinformation, missing data are equally scrutinised. If you have received funds toward your deposit, the lender may require a letter confirming that the amount is a genuine gift and doesn’t need to be repaid. A confirmation of insurance and income verification documents, including pay stubs, employment contracts, tax returns, or financial information, is vital to ensure suitability.

During the loan approval process, inspections are done in detail. Double verification is common when lenders want to confirm your employment and income with your respective employers. If a large, unexplained deposit in your bank account raises questions, lenders often require documentation citing the source.

Also Read: Understanding Debt to Income Ratio in Australia.

What Happens After a Conditional Approval?

With the notice of a conditional approval, you soon find out what happens next. All prerequisites will be promptly provided. Your first step is to address these conditions as quickly as possible to keep your loan moving forward.

The requests can range from requiring verification documents and missing data to explanations for large deposits. You would need to supply updated bank statements and tax returns. If your lender flagged unusual deposits or withdrawals, you may need to clarify the exchange. Home appraisals or inspections could also be required. Last but not least, if the title search reveals liens, judgments or ownership disparities, these must be addressed before your loan can be processed.

Did you know that the approval rate for bridging loans is faster than that of any standard loan? Purchase your new home before selling the old one with bridge loans!

If you need time to gather documents or resolve issues, an extension can be requested. However, completing these tasks promptly is duly advised. Once all conditions are verified, your loan is fully approved and ultimately moves to settlement and funding.

Are you a potential home buyer looking for alternatives to secure your dream home? Learn about rent to buy schemes to see if they’re what you’re looking for!

Is Conditional Approval a Good Sign?

As discussed previously, a conditional approval is far from a guarantee, but it’s definitely advantageous. It means you’re another step closer to approval. Any feedback from your lender helps clarify your position, and this one in particular is the very bittersweet indication that you’re well on your way to securing a home loan. Not long, and you will have the full approval you’ve eagerly waited for.

A conditional approval isn’t just beneficial for borrowers, but it’s also an indication to real estate agents and sellers that you are, in fact, serious about your home enquiries. This strengthens your position when making an offer and might even leave you at an advantage during property auctions.

Another key benefit is clarity. When you’re pre-approved after a series of consultations and verifications, you have a solid understanding of what you can afford, allowing you to make informed decisions throughout the process of buying a home. Consider using our borrowing power calculator for a quick estimate before applying.

Related: How Much House Can I Afford?

With most of your financial documents reviewed as part of the conditional approval process, the path to finalisation is much faster. Real estate agents typically prefer working with buyers who have pre-approval because it shows commitment and financial readiness. Unlike a complete rejection that barely adds value to the experience, pre-approval is education and worth combined.

Moving From Conditional Approval to Unconditional Approval

Receiving conditional approval is a major milestone, but it is not the final green light. To progress to unconditional approval, you must fulfil all requirements outlined by your lender. A series of tasks, some related to your financial profile and some to the property itself, help you go from being pre-approved to fully approved.

Also Check Out: What is a Low Doc Home Loan?

- Review Your Conditional Approval Letter Carefully: Go through all the conditions listed by your lender. Those that include providing extra documents, clarification of financial transactions or meeting property-related requirements are essential.

- Gather and Submit All Required Documents: Every bit of documentation required should be gathered and submitted promptly. From updated bank statements, tax returns, and pay slips, to identification and proofing documents. Submitting these quickly keeps the process moving and avoids delays.

- Sign the Contract of Sale: Before committing to a property purchase, sign a contract that includes a finance clause and an appropriate approval deadline. This clause in particular allows you to withdraw from the contract if your loan is not approved in time.

- Share the Contract With Your Lender or Broker: Using a Mortgage Broker can be a great way to have access to the best home loan deals and speed up your home loan application. Once the contract is signed, immediately forward it to your lender or mortgage broker. They will use this to order a property valuation and proceed with the remaining assessments.

As an investor, your rental income is your greatest asset. Find out how you can calculate your rental yield to gain insight into the regular income a property is likely to generate!

- Complete the Property Valuation Process: Your lender will arrange for a valuation to confirm that the property’s value aligns with the loan amount. A satisfactory valuation is essential to move the process forward.

- Address Any Remaining Issues: If the lender raises any further questions about your employment, credit or document clarifications, respond quickly and accurately. The faster you resolve these, the sooner your application progresses. Taking too long can leave space for doubt.

- Wait for Final Assessment: Once all conditions are met, the lender will conduct a final review of your entire application, property valuation and your financial documents.

Find out how to get a home loan if you’re self-employed!

- Receive Unconditional Approval: When the lender is fully satisfied and no conditions remain, they will issue an unconditional approval, which is the final confirmation that your loan application is approved and ready for settlement.

Guarantee your home loan without an upfront deposit with Deposit Bonds!

What If You Don’t Get A Pre-Approval?

There could be various reasons why you wouldn’t get a pre-approval, from financial to property issues or inadequate documentation. It’s important to understand the reasons behind the denial and take steps to improve your chances of approval in the future.

How does a stamp duty exemption sound to you? Well, for one, it’s possible! Learn more through our article on Stamp Duty in QLD 2026.

- Review Feedback: When you don’t pass the pre-approval, you need to understand why it happened. Consult your lenders, find out what it was that caused your application to fail.

- Look into Your Financial Situation: Ensure that your income and expenses are stable and that there hasn’t been any significant change in your transactions. Also, there shouldn’t be any new debts or late payments.

- Improve Your Credit Score: Pay off existing debts on time, do not splurge in excess and avoid unnecessary new debts. With a low credit score, it can be incredibly difficult to access a loan approval because lenders will not trust you.

Want to pay off your mortgage in only 10 years? Our article on how to pay off your mortgage faster has all the tips you need!

- Consider Alternative Lenders: If you’re not getting pre-approval from your current lender, consider exploring with different lenders or loan types. Maybe what you need is a special loan type that your acquainted lenders just do not provide.

- Look into More Properties: If you’re not getting pre-approval for a home loan, you might want to consider shopping for more affordable properties or those that meet your financial criteria.

Conditional approval is a strong stepping stone, while unconditional approval is the finish line. Understanding both and knowing how to move between them puts you in control of your home-buying journey. Looking for a stress-free pre-approval? With us at Nice Loans, your trusted mortgage partner based in Brisbane, our learned professionals take care of the hard work for you. Speak with our team today and discover exactly how we can help turn your property goals into reality.

FAQ’s

Can you start looking for properties after indicative approval?

You can totally start your property search once you receive pre-approval because the bank is satisfied with your strength as a borrower and is likely to approve your loan. With a realistic idea of your borrowing power, you don’t need to waste time with properties you cannot afford. An indicative approval presents you as a serious home buyer to the real estate agents. However, you need to keep in mind that most lenders have an expiry date on pre-approvals, so you can take your time, but don’t wait too long.

Searching for properties across Queensland? Look no further, Nice Builds, a premium home builder based in Brisbane, is just the solution for you!

How long do conditional approvals last?

Conditional approvals in Australia typically last for three to six months. This duration can vary between lenders, but it is generally accepted as a standard timeframe for this type of approval.

How long is my unconditional approval valid for?

After you receive your unconditional approval, you’ll be given some time by your lender to look for the perfect property. However, dawdling won’t get you very far because the approvals do expire. Lenders typically give you between 30 to 90 days to find the right property before the approval expires.

Can a loan be denied after unconditional approval?

While it is quite rare to happen, banks can always revoke an unconditional approval even up to the day of settlement. An unconditional approval is a guarantee, as the bank agrees to lend you the borrowed amount based on whatever information you have provided. However, if the bank discovers anything amiss in your financial data or realises something significant is missing or wasn’t properly evaluated, they could halt the clearance. However, it’s totally uncommon since lenders only approve loans that have been thoroughly checked multiple times.

Consider debt recycling to reduce mortgage faster while building wealth.

What if I go through a significant financial change, either during conditional or unconditional approval?

Financial circumstances are volatile; if you’re anything but a forest dweller, your economic conditions are bound to change with time, and even for the tribes, the economy is never constant. If you experience significant changes, it’s always wise to turn to your mortgage broker for advice. Perhaps you could land a better deal than right now?