An offset account is a transaction account linked directly to your home loan that functions like a regular savings or everyday banking account; however, a powerful advantage is what sets it apart.

Instead of earning interest, as you usually would with a regular savings account, the balance in an offset account is used to reduce the amount of your home loan on which interest is calculated.

Simply, an offset account means to lower your mortgage interest rather than helping you earn taxable interest. For example, instead of paying interest on your full loan amount, the bank calculates interest on your loan balance minus your offset account balance.

Are you self-employed, wondering how to land a home loan? We have the perfect list of tips, check them out now!

A well-utilised mortgage offset account can significantly reduce the total interest you pay and may even cut years off your home loan term. This is exactly why many borrowers obsessively hunt for the best offset loan when choosing a mortgage.

With an offset account, borrowers can deposit their salary, savings, or any income directly into the account and still use it for daily expenses such as bills, groceries and transfers. Every dollar that sits in your account reduces your effective loan balance.

Many lenders, particularly in markets like Australia, offer a 100% offset account feature as part of their variable home loan packages.

Read: Understanding Loan to Value Ratio and LVR Calculation.

Using an offset is a smart way of making everyday money work harder by lowering your mortgage interest while still giving you full access to your funds. Remember, the more money you keep in your offset account, the longer you keep it there, the more you reduce your interest costs over time.

How Does an Offset Account Work?

As previously established, at its core, an offset account reduces the amount of your loan on which interest is calculated. Instead of earning interest like a regular savings account, your money directly lowers your mortgage interest.

Let’s say your home loan balance is $500,000 while your offset account balance is $20,000. Here, instead of being charged interest on the full $500,000, your lender calculates interest on $480,000. This means your $20,000 is effectively working for you by reducing your loan interest, and that too without the funds being locked away.

Are you absolutely satisfied with your home loan and do not wish to change your mortgage solution even after a property move? Well, you can! With Home Loan Portability transfer existing home loan to a new property with ease!

A mortgage offset account doesn’t function differently from an everyday bank account. You can deposit your salary, pay bills and expenses from it and also withdraw the funds at any time. However, one key difference is that every dollar in the account works to reduce your loan balance for interest calculation purposes.

If you maintain a consistent balance in your offset account, especially from the early stages of your loan, you can effectively save thousands in interest, reduce your loan term and also increase the portion of repayments going toward the principal.

Wish to build your own home but lack the funds for it? Try Owner builder home loans to help fund your self-managed builds in stages!

What are Multiple Offsets?

Multiple offset accounts allow you to link more than one eligible transaction or savings account to a single home loan. Each of these accounts functions as an offset account, and together they help reduce the interest charged on your mortgage.

Rent wherever you want while investing where you can afford by rentvesting to boost your overall capital growth!

Instead of calculating interest on your full loan amount, the lender considers the combined balance of all your linked accounts. This means your total savings across multiple accounts are used to offset your loan.

Many borrowers opt for multiple offsets because they make budgeting easier without sacrificing any of the benefits of offset account features. Not only can you separate your money into different purposes, including for everyday spending, emergency savings, and investments, but you can also remain at ease knowing that all funds still contribute to reducing your mortgage interest, just as with a standard mortgage offset account.

Have you ever thought of using your superannuation for your home loan?

How do Multiple Offsets Even Work?

It’s quite simple: when using multiple offsets, interest is calculated by pulling the difference between your total balance across all offset accounts and your loan balance.

For instance, if your home loan is $600,000 and you have three other offset accounts, one is a savings fund of $15,000, another is the emergency fund of $10,000, and the last one amounts to $5,000. Here, your total offset balance comes to $30,000; therefore, your total interest is charged on $570,000, not $600,000.

Try using our home loan offset calculator for accurate results based on your numbers!

Multiple offset accounts in Australia are typically offered with premium or package home loans. They are often included as part of the best offset loan options, although they may come with higher fees or specific eligibility criteria.

Try debt recycling and turn your home loan debt into tax deductible debt!

Key Benefits of Offset Accounts

Financial Flexibility

Unlike several other mortgage modules that claim to help you save or strategise your home loan savings, but aren’t flexible enough for the everyday household, an offset account is a breath of fresh air.

Not only can you effectively save thousands by reducing interest on your home loan, but you can also use the saved money whenever you want to, without incurring a massive loss. Even for individuals with unstable financial backgrounds, offset accounts can be perfect alternatives to save while avoiding heavy risk.

Calculate your rental yield to find your real profit after all expenses on your investment property!

Accessible Everyday Banking

One of the biggest advantages highlighted in any offset account is its flexibility. An offset account is just like your regular savings account, meaning that everything you do with a regular account, you can do with an offset.

Unlike other loan features, where there are restrictions and delays when accessing your saved money, offset accounts help you make transactions with ease. This makes it ideal for borrowers who want to grow both liquidity and savings at the same time.

Find out how much you need for a house deposit.

Better Effective Returns

Although an offset account does not pay interest like a traditional savings account, it delivers a higher return in several cases. You should know that home loan interest rates are typically higher than savings account rates, so every little amount in your offset reduces the interest charged, which means the return you’re getting is the interest saved and not earned, which amounts to a lot in the long run. This slowly helps you pay off your mortgage faster since your repayments add to the principal rather than the interest payment.

Daily Savings on Interest

Another major benefit of an offset account is how interest is calculated. Most lenders calculate home loan interest daily, which means every dollar in your account counts immediately, and even short-term deposits can reduce your interest.

Whether you save consistently or from time to time, the benefits will keep coming. Over time, the small reductions can add up to substantial long-term savings and can even shorten your loan term.

Land your dream home with zero deposit on your home loan!

Tax Efficiency

One of the most overlooked advantages of an offset account is its tax efficiency. With an offset account, since you are not earning interest but instead saving interest on your loan, the savings are generally not taxed.

This means your effective return from an offset account is often higher after tax compared to that of a savings account. For borrowers who are subject to higher tax brackets, this mortgage offset account becomes an even more powerful financial tool.

Buy a new home before selling your current one with bridging loans!

Offset Account Disadvantages

While the benefits of offset account features are compelling, it’s equally important to understand the potential downsides before choosing one.

Try Trust Home Loans to purchase property through a trust while improving asset protection and tax flexibility!

Higher Fees Can Reduce Savings

One of the main offset account disadvantages is the additional cost involved in setting it up. Several lenders bundle offset accounts with premium home loan packages that include monthly account fees, annual package fees and high service charges. While the mortgage offset account can save you interest, those savings can be reduced or even eliminated if the fees are too high.

Therefore, it is advised that you calculate the total interest saved vs the total fees required to set up the offset account and decide accordingly.

Higher Interest Rates on Offset Loans

Another key drawback is that loans with offset features often come with slightly higher interest rates compared to basic home loans. Which means that you may need to pay more interest on the loan itself while making sure that the offset benefit outweighs the higher interest rate.

Remember, to always look beyond the feature itself and evaluate the total cost of the loan. In several cases, a lower-rate loan without an offset may actually be cheaper overall.

Are you buying your first home? Learn more about first home buyer grants and schemes to get heavy discounts on your mortgage!

A Significant Balance is Required For It to Be Effective

An offset account means your savings reduce your loan interest, but the impact depends heavily on how much money you keep in your account. If your balance is low, the interest savings will be minimal, and fees and higher rates may outweigh the benefit.

To truly maximise a mortgage offset account, you typically need a savings buffer that is pretty consistent or a large sum sitting in the account. Without this, the feature may not justify its cost.

Figure out your home affordability to estimate an accurate budget for your home loan!

Not all Offset Accounts are the Same

Not every offset account offers the same value. Features and conditions can vary significantly between lenders. Before you assume one to be the best offset loan, always review the fee structures, interest rate differences, withdrawal rules and also the number of offset accounts allowed. Understanding these details is crucial to ensuring the offset account actually works in your favour.

Rent now with the option to buy later with Australian Rent to Buy Schemes!

Strict Financial Discipline is Required

While this cannot be considered much of an offset account disadvantage, it is a hard brick to crack. Since your offset account works like a regular transaction account, it’s easy to spend from it, and these frequent withdrawals can reduce your effective savings. Which means, your loan interest increases as your balance drops.

If you regularly dip into the account for everyday expenses without maintaining a healthy balance, you may not experience the full benefits of offset account usage. Without financial discipline, your efforts will only go in vain.

Refinance your home loan for better loan rates and features!

How Can You Make the Most of Your Offset Account?

An offset account is one of the most effective tools for reducing mortgage interest, provided it is used strategically. If you’re wondering how an offset account works in practice to deliver real benefits, your answer lies in how consistently and intelligently you use it. Below are some of the most effective ways to maximise the benefits of offset accounts:

Use Your Offset Account as a Primary Bank Account

One of the smartest strategies to maximise offset account benefits is to treat it as your main everyday account instead of a regular savings account. This means depositing your income into the offset, paying your bills and expenses from it, basically ensuring that you keep all your cash flow within the account.

When you do this, your entire balance is constantly working to reduce your loan interest. This approach reinforces what an offset account means inherently; every dollar sitting in your account is actively lowering your mortgage cost, even when it is fully accessible.

Did you know that a guarantor can boost the approval chances for your home loan? Get one now!

Deposit Your Salary Directly

To maximise savings, have your salary paid directly into your offset account. This works because your full income starts offsetting interest immediately, even if you spend it later, you still benefit from daily interest reduction.

Ask your mortgage broker these 20 burning questions!

Keep as Much Money as Possible in Your Offset

Because interest is calculated daily, every dollar, every day counts. Even small balances can help reduce your interest, so try to stay consistent with your inputs and aim for long-term savings that can compound over time.

Try understanding the difference between conditional and unconditional approval to meet lender conditions effectively!

Try Not to Withdraw Too Much and Maintain a High Balance

The more money in the offset and the longer you keep it there, the more interest you save. Frequent withdrawals reduce your effective balance, which increases the interest charged on your loan.

To maximise returns, you need to keep a consistent savings buffer and avoid unnecessary spending from the account, and if possible, try using multiple offsets through which you can separate the spending money.

Secure your dream property without an upfront deposit with deposit bonds!

Try Using a Loan Repayment Calculator to Plan Your Savings

If you wish to fully understand how an offset account works financially, using a loan repayment calculator can prove beneficial. Our loan repayment calculator allows you to adjust the loan amount, term and interest rate. You can also estimate your average offset balance and see how much interest you could save. This helps determine whether you’re choosing the best offset loan and how to optimise your strategy over time.

Maximise the Power of Multiple Offset Accounts

If your lender allows it, using multiple offset accounts can significantly improve both organisation and savings. You can split your finances into everyday spending, emergency funds and long-term savings. Even though the funds are separated, they all contribute to reducing your loan interest. This makes budgeting easier while still delivering the full benefits of offset account functionality.

Also Read: Lenders Mortgage Insurance (LMI): Everything You Need to Know.

How Not to Use Your Offset Account?

While an offset account can be a powerful tool for reducing mortgage interest, using it incorrectly can significantly limit its effectiveness. You should also know that your financial background, your credit history and score also have a huge effect on whether you will be allowed an offset account or not. Utilising an offset account properly isn’t just about what to do right, but also about understanding what to avoid.

Get a buyer’s agent to do property negotiations for you!

Here’s a list of all things to avoid:

- Do not treat your offset account like a regular transaction account.

- Do not link your everyday debit card to your primary offset account.

- Do not leave your account on a low balance without regularly depositing funds.

- Do not make frequent withdrawals.

- Do not overlook fees and overall costs.

- Do not mix personal and investment property or miscellaneous investment funds; tax treatment can vary depending on how a loan is structured. Seek professional advice.

If you’re self-employed or a non-traditional earner, a low doc home loan offers you just the flexibility you need!

Offset Account vs Normal Savings Account

When comparing an offset account with a normal savings account, it’s important to understand how each option makes your money work and which one delivers better financial outcomes over time.

Basically, both accounts function similarly; both allow you to store and access your money, but the way they generate value is fundamentally different. First off, in a savings account, your money earns interest at a fixed rate, whereas in an offset account, your money reduces the interest charged on your home loan.

One of the biggest differences between the offset account and the savings account is taxation. Savings account interest is treated as taxable income, while offset account savings are not taxed because here you’re not earning interest, you’re reducing it.

Buy your dream home at only 2% deposit with the Australian Help to Buy Scheme!

With both accounts, you can access your savings, make deposits and withdrawals as you wish. But offset accounts have an added advantage, which is that it simultaneously reduces your mortgage interest while letting you use the saved funds and add more.

Offset accounts can come with account fees, annual package fees and slightly higher home loan interest rates, whereas savings accounts have low or no fees at all and offer lower returns in comparison.

Ultimately, when it comes to choosing the better option, there is no one-size-fits-all answer. However, depending on your needs and circumstances, one can be better for you than another.

Check Out: Stamp Duty in QLD 2026!

Offset Account vs Redraw Facility

What exactly is a Redraw Facility? A redraw, unlike an offset account, is a home loan feature where extra repayments are made directly into your home loan, and these funds help reduce your loan principal. You may be able to withdraw these extra repayments later; however, access to these funds depends on your lender’s rules.

Both the Offset Account and the Redraw Facility help reduce the interest you pay, but in different ways. An offset account reduces the effective loan balance, while the redraw facility reduces the actual loan balance.

From an interest perspective, the outcome can be similar, but the access and flexibility differ significantly. Where you can get instant access to your offset account funds, the redraw facility may have withdrawal limits and require approval or processing time.

Are you a single parent looking for a home loan? The family home guarantee scheme helps you buy with a low deposit and zero LMI!

A redraw facility may limit the number of redraws and charge fees per withdrawal, whereas offset accounts provide full transactional capability and real-time access to funds. The tax treatment can differ, especially for investment properties. Offset accounts generally offer better flexibility for tax structuring, but redraw facilities can create complications if funds are withdrawn and reused.

In the end, there is no universal answer in the offset account vs redraw facility debate; the choice depends on your financial behaviour and goals. An offset account may be better if you want full access to your money or want to manage daily cash flow actively; however, if you prefer forced savings, don’t need frequent access to your funds and only want a simple, lower-cost loan structure, a redraw facility can be the solution for you.

Easily access your home equity without selling with a reverse mortgage or other home equity release options!

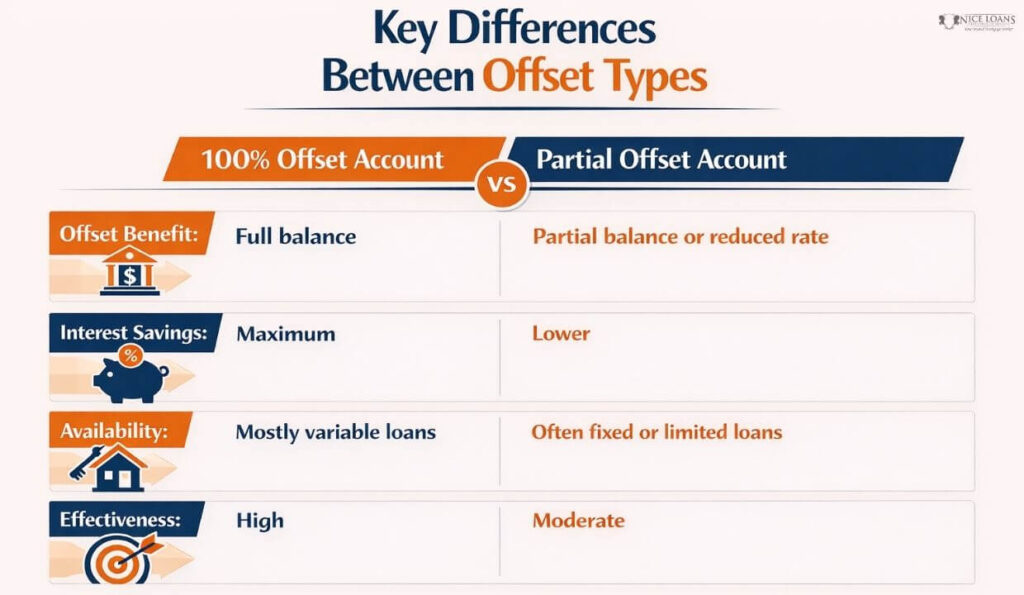

Types of Home Loan Offsets

Broadly, offset accounts fall into two major categories, namely 100% offset accounts and Partial Offset Accounts.

- 100% Offset Account: Also known as a full offset, the 100% offset account is the most common and effective type of mortgage offset account. Here, every dollar in your offset account is fully deducted from your home loan balance when calculating interest. Which means your savings are working at the same rate as your home loan interest, making it highly efficient.

Wish to refinance but have low credit? Don’t panic because with certain effective strategies its possible!

- Partial Offset Account: A partial offset account provides a reduced level of benefit compared to a full offset. There are two common variations here: reduced interest offset and percentage-based offset. In a reduced interest offset, your offset balance earns a lower offset rate, which is less than your home loan interest rate, whereas with a percentage-based offset, a less common structure, only a portion of your balance offsets your loan. This type of account is sometimes offered with fixed rate loans over variable rate loans, where offset features may not be available.

Is an Offset Account the Home Loan Solution for You?

Deciding whether an offset account is the right home loan solution for you depends on your financial habits, loan size and ability to maintain savings. While a mortgage offset account can be a powerful tool, it isn’t automatically the best option for everyone.

An offset account can be highly beneficial if you have a large home loan, where even small reductions in interest can lead to significant savings. However, if you have a low balance and the loan you’re taking comes with higher interest rates compared to standard home loans, it might not be the solution you’re looking for.

Lastly, since every financial situation is different, it’s often a good idea to seek guidance before choosing a loan with an offset feature. Consider speaking to a mortgage broker or a lending specialist who can help you compare loan features and evaluate fees vs savings.

Get in touch with our team at Nice Loans, your trusted mortgage brokerage based in Brisbane, for unbiased home loan advice. Together with us, you can carefully consider your financial behaviour and compare options that will help you decide on the perfect economic future.

FAQs

How much can you save with an offset account?

The amount you can save with an offset account depends on your loan size, interest rate and how much money you have in your offset account. If used properly, the return from an offset account can often outperform the return from a regular savings account.

Can you offset 100% of my mortgage?

Yes, a 100% offset is possible. If your offset balance is equal to your loan balance, you will pay zero interest for that particular period.

Find out what happens on settlement day to avoid mishaps and stress!

Does an offset account reduce repayments?

No, offset accounts do not reduce repayments. However, they do reduce the interest charged on your loan, and more of your repayment goes toward the principal.