With the spring selling season just around the corner, here’s what’s making news in the mortgage and property markets:

- Rental market cools

- 3% mortgage buffer explained

- Borrowing rises 19.1%

- Construction loans explained

Read more below.

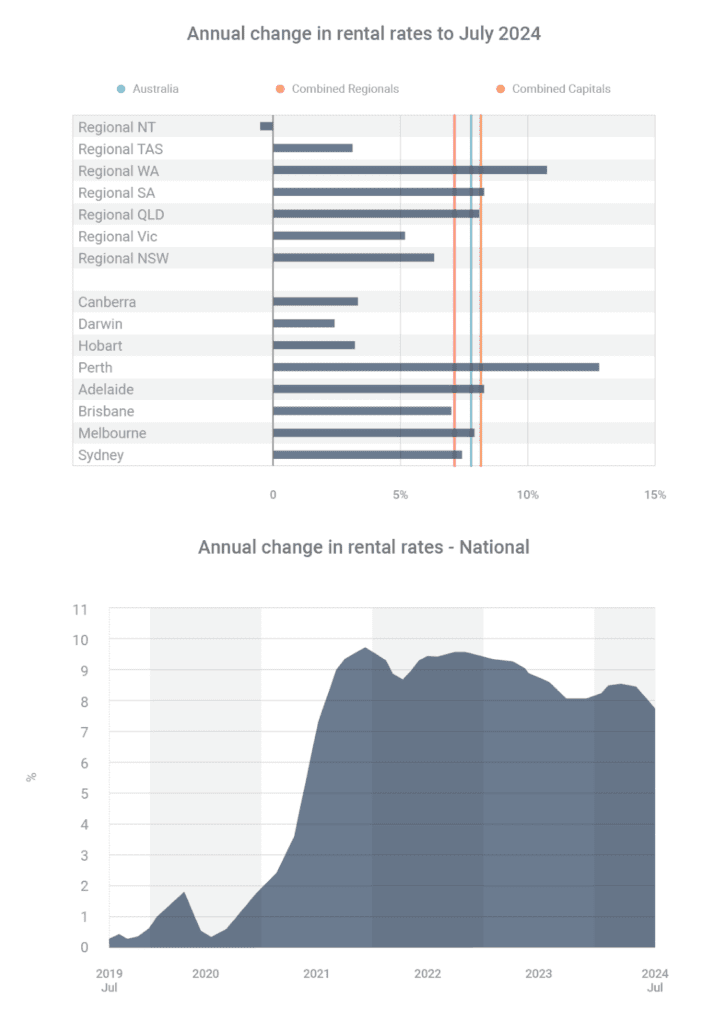

Property investors have enjoyed a golden run over the past five years, during which the national median rent increased 39.7%. However, in July, rents increased just 0.1%, which was the slowest growth since 2020, according to CoreLogic.

At the same time, annual rental growth has been trending down over the past few months.

Between February and July, rental growth fell from 9.7% to 8.0% in the combined capitals, although it rose from 5.4% to 7.1% in the combined regions. The big cities appear to be close to their rental affordability limit, while the regions, which have had less rental growth, might have more capacity to absorb higher rents.

Despite the slowdown of the national rental market, CoreLogic economist Kaitlyn Ezzy said rents were likely to keep increasing.

“Low supply will likely continue to put upward pressure on rents, albeit at a slower pace,” she said.

“With dwelling approvals and commencements at historic lows, providing sufficient new housing will not be a quick fix and remains a genuine challenge for policymakers, the property industry and, of course, tenants.”

In other words, while rents are likely to keep rising, tenants are likely to get some relief and investors shouldn’t budget for the double-digit-percentage increases of previous years.

When you apply for a mortgage, the lender uses a series of criteria to assess how likely you’d be to repay the loan. As part of this process, the lender also considers whether you’d be able to continue making your repayments if interest rates were to rise.

Generally, lenders will apply a buffer of at least 3.00 percentage points – so if you applied for a loan with an interest rate of 6.50%, this would mean calculating whether you’d be able to make repayments at 9.50%.

This ‘mortgage serviceability buffer’, as it’s known, is mandated by APRA, Australia’s banking regulator.

Partly, it’s designed to prevent lenders from issuing risky loans; because if a large number of borrowers defaulted on their loans, that would undermine the banking system. And, partly, it’s designed to protect borrowers from taking on loans they might not be able to afford.

The serviceability buffer can make it harder for borrowers to qualify for loans, but is ultimately designed to be in their best interests.

TALK TO ME ABOUT YOUR BORROWING

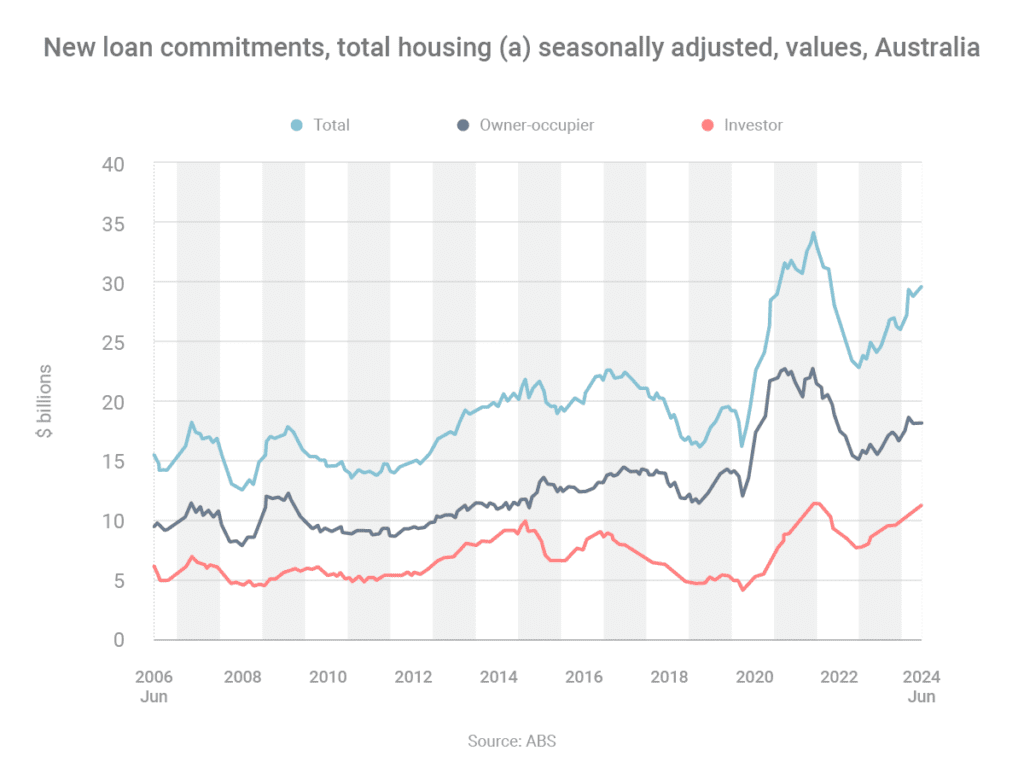

The latest home loans data from the Australian Bureau of Statistics has revealed three key trends.

- Borrowing is rising strongly. The total value of home loan commitments in June reached $29.19 billion, which was 1.3% higher than the previous month and 19.1% higher than the previous year.

- Investor activity is incredibly strong right now. While the volume of owner-occupied loans rose 13.2% year-on-year to $18.17 billion, investment loans jumped 30.2% to $11.02 billion.

- While refinancing activity remains quite high, it’s well below the record levels of mid-2023. Borrowers refinanced $15.79 billion of loans in June, which was 20.9% lower than the year before.

Contact me if you’re thinking about buying a property. I can get you a home loan pre-approval and, if you’re interested, introduce you to a good buyer’s agent.

One of the great things about constructing your own home is that it can be tailored to your specifications. If you’re interested in building rather than buying your dream home, here’s the process you need to follow:

- Speak to your broker about your goals, so you can create a finance plan together

- Buy the land

- Design your home

- Find a reputable builder

- Obtain building permits and approvals

- Build the home

With a traditional home loan, you receive the money in one lump sum; but with a construction loan, you receive the money in five stages throughout the project. You pay interest-only on the portion of the funds you’ve received to date, rather than the whole loan; and at the end of the build, your loan reverts to a traditional principal-and-interest mortgage.

It’s worth noting that the rate of annual growth in house-building costs increased from 3.9% in September 2023 to 4.3% in June 2024, according to the Australian Bureau of Statistics.

Given that costs will likely continue to rise, the sooner you build, the cheaper it could be in the long term. If this is something you’re thinking about doing, you should explore your options soon.

GET IN TOUCH IF YOU NEED A CONSTRUCTION LOAN

I can help you buy a home, build a home, purchase a vehicle or refinance an existing loan, so please get in touch if you need assistance.