In this month’s newsletter, you’ll find some interesting insights about the rise in borrowing activity, the federal government’s housing assistance program and the spring surge in listings:

- 35.4% jump in investor lending

- Govt scheme helping ten of thousands of buyers

- More choice for buyers as listings rise 7.9%

- Why buy & hold can be a lucrative state

Read more below.

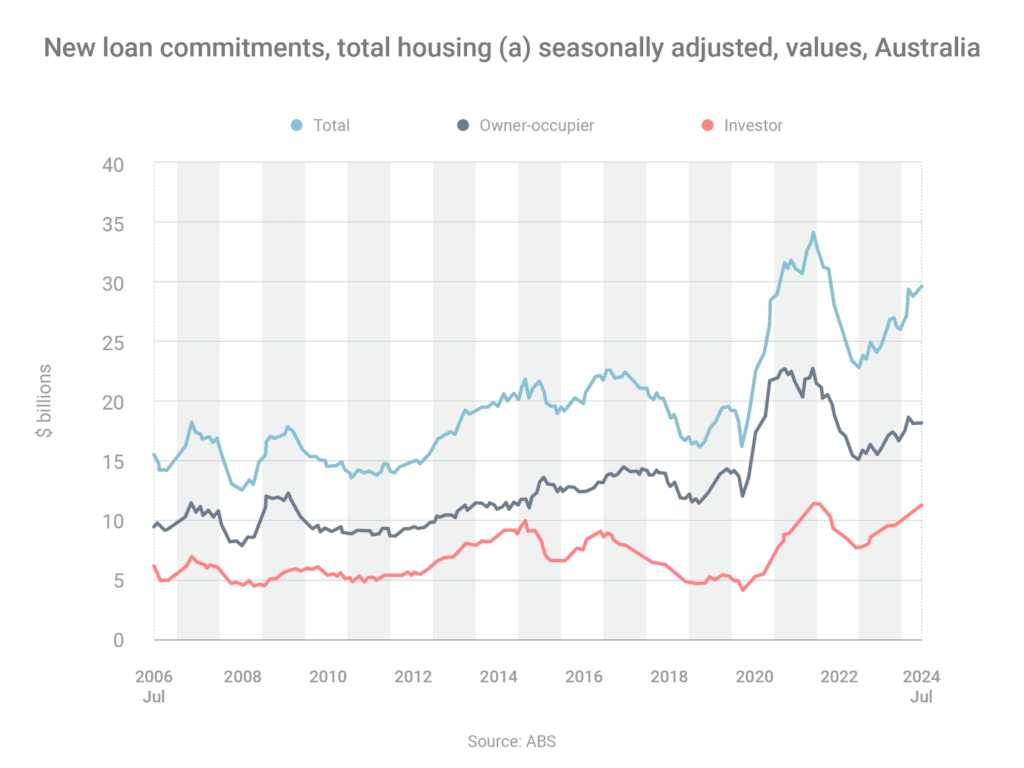

Property investors committed to $11.71 billion of home loans in July 2024, which was the second-highest month on record, according to the Australian Bureau of Statistics.

It was also 35.4% higher than in July 2023, showing the enormous growth in investor activity during that time.

Here are five reasons why so many Australians consider property investing a great way to build wealth:

- Capital growth – property prices have increased significantly over the long-term

- Rental income – the income you collect from your tenants can contribute to paying off your mortgage

- Tax benefits – you can potentially reduce your taxable income if your expenses exceed your income

- Diversification – property can balance out any shares you may own through your superannuation

- Flexibility – once you’ve accumulated enough equity in your investment property, you can use that to fund the deposit on another property

As you can see, property investing has a lot of potential benefits. If you want to know more, I’ll be happy to run some numbers for you.

Let’s talk property investment

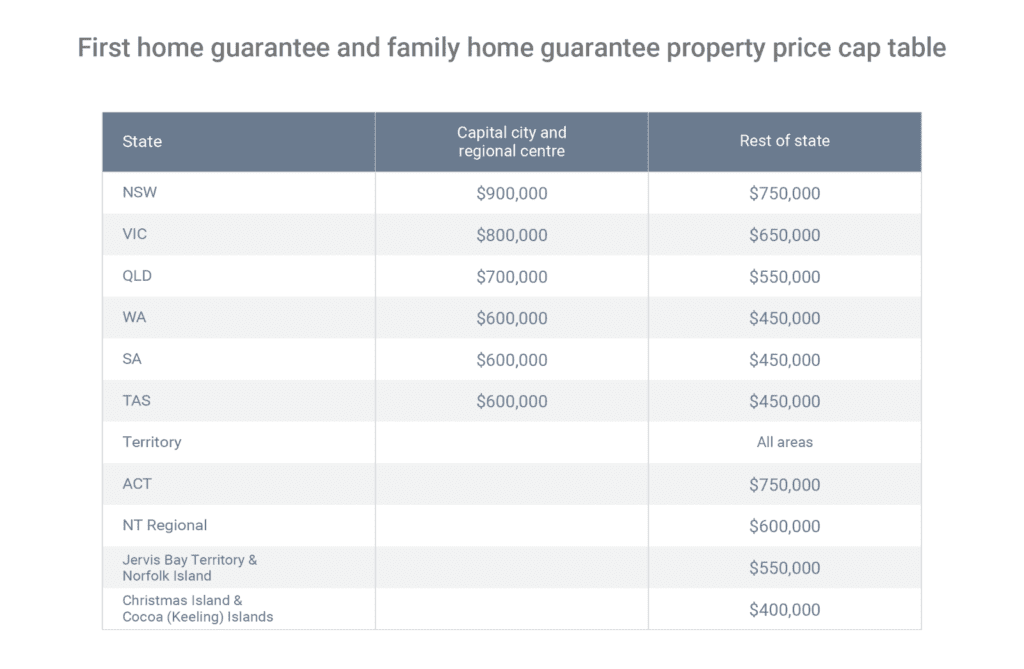

The federal government’s Home Guarantee Scheme (HGS) helped 43,800 buyers enter the market in the 2023-24 financial year, Housing Australia has revealed.

The HGS contains three separate programs:

- The First Home Guarantee helps eligible first home buyers, and people who haven’t owned a home for at least 10 years, to purchase a property with a 5% deposit without paying lender’s mortgage insurance (LMI)

- The Regional First Home Buyer Guarantee is almost identical, but is limited to regional buyers purchasing regional properties

- The Family Home Guarantee helps eligible single parents and single legal guardians buy a property with a 2% deposit without paying LMI

The federal government has allocated a combined 50,000 places for the three programs in the 2024-25 financial year.

All three programs are reserved for owner-occupiers, have income limits ($125,000 for single applicants and $200,000 applicants) and property price caps (see table above).

Please contact me if you’re thinking about taking advantage of the HGS. I can advise you if you meet the eligibility criteria and manage your home loan application.

Want to learn more about the HGS? Let’s talk

Home hunters have considerably more stock to choose from than earlier in the year, putting buyers in a stronger negotiating position.

SQM Research has reported that the total number of listings across Australia in August was 7.9% higher than the month before and 11.1% higher than the year before, while the number of new listings (those less than 30 days old) rose 11.8% month-on-month and 8.5% year-on-year.

“Going forward, the spring selling season will provide a significant level of choice for buyers, particularly in Sydney and Melbourne, with listings at their highest levels in some years,” according to SQM Research.

This is good news if you’re thinking about buying a property, because it means you’ll face less competition from other buyers. But it’s not such good news if you’re thinking about selling, because you’ll face more competition from other sellers. As a result, buyers will be encouraged to make lower offers and sellers might be forced to settle for less.

About 20% of home owners bought their property in the past five years, CoreLogic has estimated. The data shows that 2021 was the most common year in which homes were last purchased, with 5.3% of all homes being bought in that year.

It makes perfect sense for people to buy and sell homes every few years, because as circumstances change, we may need to upgrade, downgrade or relocate. That said, if you are able to hold onto a property for the long-term, there can be enormous benefits.

First, you can avoid the transaction costs associated with buying and selling. Second, you can potentially enjoy strong capital growth. CoreLogic reports that the nation’s median property price has increased by 70.2% over the past 10 years, 157.9% over the past 20 years and 425.9% over the past 30 years.

Depending on your financial circumstances, it might be possible to move without selling your existing home if you turned it into an investment property. While you’d then have two mortgages, some of that extra cost would be offset by the rent you’d start collecting.

If you want a larger or newer home, another alternative would be to renovate instead of moving: potentially, you could finance the project by borrowing against the equity in your home.

The spring season is often the busiest time of the year, with a lot of buying activity taking place. Reach out if you’d like me to secure a home loan pre-approval for you or to refinance an existing loan.