The new financial year is almost upon us – I hope your business had a great year. I’ve put together a few insights into the Australian economy and commercial property market that could help you plan for a strong FY26.

- How to thrive in a weak economy

- ATO interest no longer tax-deductible

- Office vacancies affecting parking rates

- RBA open to rate cut stimulus

Read more below.

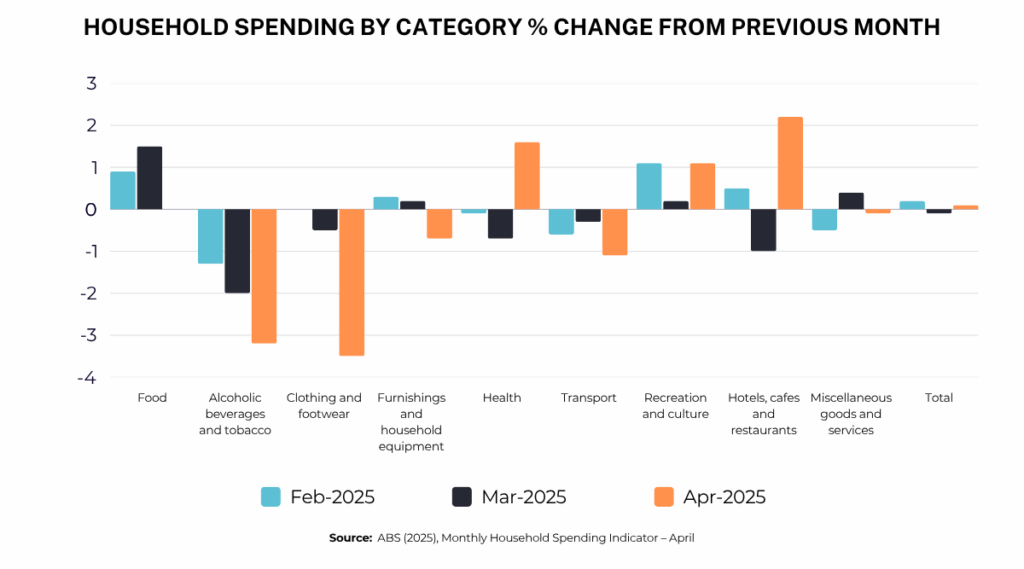

Consumers are reluctant to open their wallets, leading to challenging conditions for businesses.

Household spending in April was just 0.1% higher than the month before, while retail spending was actually 0.1% lower, according to the latest data from the Australian Bureau of Statistics.

This cautious spending behaviour is reflected in the household saving ratio, which has risen for three consecutive quarters. In June 2024, households saved an average of 2.4% of their income. That figure rose to 3.7% in September, 3.9% in December and 5.2% in March 2025.

Weak spending is a double-edged sword for businesses. On the one hand, it puts downward pressure on inflation; on the other hand, it means lower sales.

Here are five ways your business may be able to raise sales in the 2025-26 financial year:

- Improve your online presence. Ensure your website is up to date, mobile-friendly and easy to navigate.

- Invest in customer retention. It’s often cheaper to keep existing customers than win new ones – consider loyalty programs or personalised offers.

- Review your pricing strategy. Small adjustments or bundled deals may help you appeal to more cost-conscious consumers.

- Diversify your marketing. Use a mix of channels – like email, social media and local partnerships – to reach different audiences.

- Offer flexible payment options. Buy-now-pay-later services or extended terms may encourage spending during tighter economic times.

From 1 July 2025, the interest charged by the Australian Taxation Office (ATO) on overdue tax debts will no longer be tax deductible.

Until now, some business owners have treated the general interest charge (GIC) – currently 11.17% and compounding daily – as a manageable expense. But from the 2025–26 financial year, that interest will increase your costs without reducing your tax bill.

To avoid getting stung, it’s wise to:

- Pay your ATO debt as soon as possible. If you can’t pay it in full, consider setting up a short-term payment plan.

- Speak to your accountant about lower-interest options. A business loan or line of credit might be a more tax-effective way to manage cash flow.

- Plan ahead by setting aside funds for GST, PAYG withholding and superannuation each month.

Staying on top of your tax obligations will allow you to avoid interest altogether. But if that’s not possible, taking action now could save you money next financial year.

Australia’s parking market reflects wider economic shifts, with city-to-city differences revealing where office markets are recovering – and where they’re still struggling.

Brisbane has overtaken Sydney as the country’s most expensive city for casual parking, with average daily rates of $80.84, according to Ray White Group. Vanessa Rader, Ray White Group’s Head of Research, said the high cost was linked to stronger office attendance.

“Brisbane’s office vacancy rate is just 10.2%, and we’ve seen positive take-up of space,” Ms Rader said. “That demand is supporting premium pricing.”

By contrast, Melbourne’s parking prices have gone backwards. Daily rates now sit at $64.43 – lower than they were in 2013 – which Ms Rader said reflected poor office conditions.

“Melbourne has the highest vacancy rate of any capital at 18.0%. That’s why parking operators have introduced the deepest early bird discounts in the country – 62.9% – to maintain cash flow,” she said.

Across the country, operators are adjusting their strategies based on market conditions, offering heavy discounts in weaker CBDs and more modest incentives in stronger-performing capitals.

Get in touch if you’d like to finance the purchase of a commercial parking asset.

The Reserve Bank of Australia (RBA) believes the local economy is softening, although domestic conditions have generally evolved in line with expectations.

In the minutes of its latest monetary policy meeting, on 19-20 May, the RBA noted that GDP growth had picked up in late 2024, but early 2025 data showed household consumption was weaker than expected. “Earlier declines in real household disposable income remain a constraint on consumption,” the RBA said, although rising wealth had provided some support.

Business sentiment and hiring intentions remain broadly stable, and unemployment has held at about 4.1% since mid-2024. However, wages growth has softened and voluntary job turnover has declined, pointing to reduced confidence among workers.

The RBA welcomed progress on inflation, with the trimmed mean measure returning to the target range of 2-3%. “This path had been expected, but it provided welcome confirmation that potential upside inflationary risks had not crystallised,” it said.

At the meeting, the RBA cut the cash rate by 25 basis points, bringing it to 3.85%, and signalled it was prepared to cut again if downside risks from global developments were to materialise.